Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

– Use USD/ZAR DCS for hedging - EconoTimes)

The most recent South African economic data was not exactly constructive: the unemployment rate rose to over 27% in Q3 and the inflation rate also rose to 6.4% in October. That means it has eased only slightly against its high in February of 7% and remains stubbornly above the central bank’s target corridor of 3-6%.

The South African Reserve Bank left its benchmark repo rate on hold at 7 pct at its November of 2016 meeting, as widely expected.

Policymakers said growth in the third quarter is expected to be positive, but below the level of June quarter, while left the GDP forecasts unchanged from September. The inflation reached to an 8-month high in October, after food prices picked up the most since 2009 due to severe drought, but it is expected to moderate in early 2017.

The bank also noted the rand will be sensitive to changes in the stance of the US monetary policy.

The central bank (SARB) now seems to be increasingly stuck between a rock and a hard place in the shape of the weak economic data on the one hand and the increased depreciation pressure on the rand on the other.

After all, in its October report, it expected the rate of inflation to return into the target corridor in the second quarter of 2017.

However, the biggest risk in this context is the rand. In addition to global factors, it is mainly the political uncertainty in South Africa that is putting pressure on the rand as well as the risk of a rating downgrade.

We firmly maintain our bearish stance in ZAR, with the South African rand screening as exorbitantly priced versus the dollar, even as the domestic political story has suffered a meaningful shift. The rand now appears to be pricing in “positive" political risk premium, as recent events have weakened President Zuma’s position and increased the chances of a “regime change”.

The current market price action differs from previous political episodes, where USDZAR has frequently priced negative political risk premium related to risks that Finance Minister Gordhan could be dismissed.

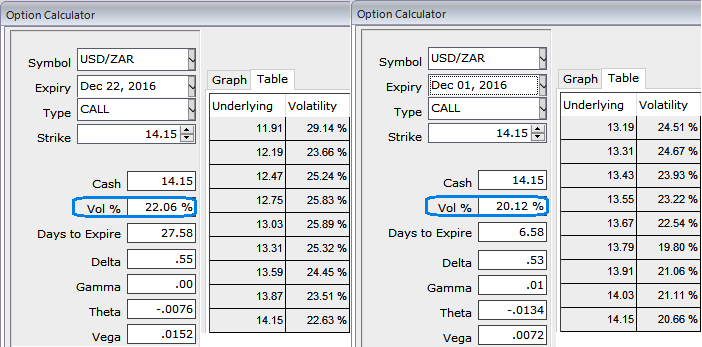

FX Option Strategy - Diagonal Call Spreads (DCS):

Hence, we upheld the long positions in USDZAR in option spreads, cash trades were not preferred on account of high yield IVs, 1m ATM IVs are spiking shy above 22% from 20% in 1w tenor which is a good sign for option holders.

Anticipating further price upswings in the underlying spot of USDZAR, on hedging front, we recommend positioning long USDZAR (ZAR has been significantly overshooting fundamentals), which makes buying USDZAR vol all the more appealing.

In a naked vanilla form, we suggest credit call spreads types at the 1M horizon but with a diagonal tenor pattern, optimizing strikes for leverage. In USDZAR, the 1M-2MATM spread is below average at +0.75, as 1M vols had remained relatively anchored and never softened significantly. One could initiate their option trades as shown in the diagram, but use appropriate strikes and tenors as per the requirements.