Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis

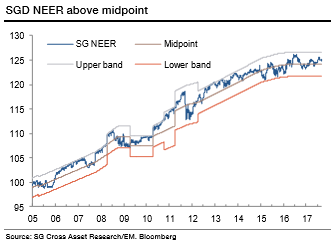

It is believed that SGD would be a regional underperformer and should be used as a funding currency. The chance of the MAS tightening policy is very low and instead we assign a 70% chance that the midpoint of the SGD NEER will need to be re-centered over the coming years.

The economy will likely remain mired in a low growth and low inflation environment due to:

1) The downside risks to Chinese growth in 2018,

2) The weak productivity and slow growth in the labour force,

3) A muted consumer credit cycle,

4) The weakness in property price, and

5) The reduced inflow of foreign labour.

Key drivers: As long as the EUR remains bid, the USDSGD will creep lower. However, assuming the MAS does not tighten in October and Chinese growth starts to slow, the SGD NEER should settle at the bottom of the band.

Risks: Surprise hawkish rhetoric or a tightening of policy (i.e. moving to an upward slope) would shift the SGD’s dynamics to that of an outperformer.

In EM Asia, we hold OW MYR and short USDSGD. Skew: KRW has high skew and high skew-to-vol (call spreads offer attractive discounting for dollar bullish views) – these metrics are very low in SGD and CNH. Convexity: Butterflies are expensive in KRW and cheap in CNH, SGD, TWD, INR, in our view. Use 1m debit put spreads for USDSGD downside risks.