BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

The CBRT let down analysts at its recent monetary policy meeting keeping the policy rate on hold at 17.75%. The analyst consensus, as well as market pricing, was for a 100 bps hike.

The Turkish central bank elucidated status quo decision by figuring out “a more significant rebalancing trend in economic activity” while signifying that “lagged impact of recent monetary policy decisions” and “contribution of fiscal policy” will help this rebalancing.

On the flips side, with this decision, CBRT failed to counteract the upside surprise in the June inflation print. Headline inflation jumped to 15.4% YoY in June from 12.2% YoY in May.

Geopolitical headwind: In the recent past, the US President Donald Trump announced "large sanctions" against Turkey yesterday via Twitter - in retaliation for the arrest of a US citizen. Well, the Turkish government has shown some flexibility (and sufficient influence on the judiciary) in similar cases in the past.

A solution to this dispute, therefore, seems possible. The fact that the Lira still dropped significantly may be due to the fact that it is already vulnerable after Tuesday's central bank decision. Every TRY-negative news flow has an intensified effect.

In such a situation, US sanctions - even temporary ones - would be dangerous. They would increase the risk of a spiral of TRY depreciation and capital flight.

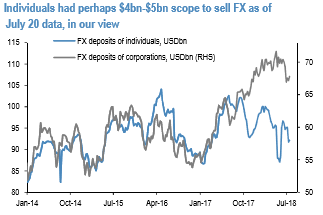

We believe the lira will sell-off further despite the muted reaction so far. The currency reacted negatively on the day but hasn’t sold off substantially yet. The retail sector still has some scope to sell FX but not large. We believe the retail sector had about $4bn$5bn scope to sell FX further as of data available up to July 20. We arrive at this figure by assuming individual investors can run down FX balances towards the low end of their recent range (refer 1st chart). However, some of this selling buffer was likely already used after the CBRT decision and hence it is again smaller now. Meanwhile, we do not assume any further scope for corporates to sell given that they currently hold only marginally more than their short-term FX liabilities.

NDF auctions now do not provide any further support to the currency and neither do rediscount credits. The NDF auction schedule now shows a flat profile for Q3 (refer 2nd chart), in line with CBRT signalling a $10bn cap for the program. This program provided about $2.4bn support to the market in June.

Meanwhile, CBRT allowing corporates to repay the rediscount credit program in lira provided up to $2n support to the FX market in both June and July (partially explaining the drop in FX reserves, refer 3rd chart). But the support from this program is now also ending. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index is flashing at -56 levels (which is bearish), while hourly EUR spot index was at 37 (mildly bullish) while articulating at (13:45 GMT). For more details on the index, please refer below weblink: