Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Before we begin with this write-up, please go through our previous article on this pair:

We had advocated a hedging piece on any abrupt CNH appreciation, accordingly, you could observe since January 3rd CNH gained substantially.

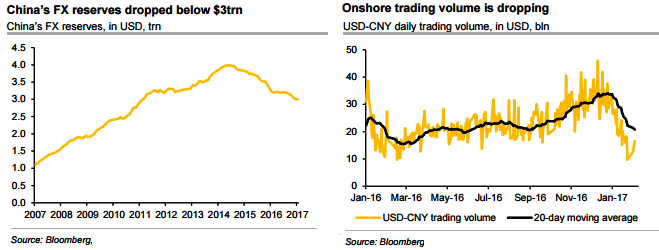

The China’s FX reserves dipped below the USD3trn watermark in the first month of 2017. Indeed, China has burnt down USD1trn FX reserves to conduct direct FX market intervention since mid-2014. However, this has not changed the market expectations over CNY exchange rates.

FX reserves dipped to below $3trn China’s FX reserves dropped below the psychological level of USD3trn at the end of January, at USD2.998trn, from USD3.01trn in the prior month. This is the first time since February 2011 that China’s FX reserves have fallen below USD3trn. Clearly, capital outflow pressures remain despite the presence of supportive factors.

First, EUR and JPY appreciated 2.7% and 3.7% against the USD respectively in January, which should increase China’s FX reserves to gain USD30bln from a valuation perspective (we assume that 2/3 of China’s FX reserves are in USD, 20% in EUR, 10% in JPY).

Second, China’s central bank actually reduced the outright intervention in both onshore and offshore markets over the past few months, which should have helped to slow down the decline of reserves. Instead, they conducted administrative measures to reduce USD purchase flows in the onshore market, while increasing the cost of shorting CNH in the offshore market to fight against market speculators;

Third, due to Chinese New Year holidays, there were fewer trading days in January, and the corporates are normally less active during holiday seasons. In fact, the trading volume on the onshore market also dropped dramatically in January.

(Refer above chart) Nonetheless, the fact that China holds less than USD3trn FX reserves right now means that China has to rethink its intervention strategy. Since mid-2014, China’s central bank has burnt down almost USD1trn FX reserves to conduct the market intervention. However, it does not make too much sense as the market expectations are unlikely to be changed.

Well, for now, we advocate upholding below hedging vehicles:

Buy USDCNH 1y topside seagull, strikes 6.80/7.20/7.50, zero cost (indicative, spot ref: 6.8330), the structure is a standard 1y call spread strikes 7.20/7.50 fully financed by selling a put strike 6.80, exposed to a maximum USDCNH appreciation of 4.2% at expiry.