Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data

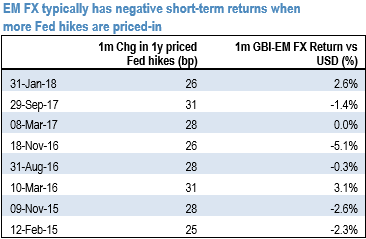

The short-term repricing of Fed hikes is typically not supportive of EM FX returns, which also motivates our selective hedges (e.g. TRY and MXN). The recent research in the past emphasized the distinction between increases in core yields driven by rising breakeven inflation (good bond sell-off) versus rising real yields (bad bond sell-off).

The above nutshell illustrates the episodes since 2013 that saw another Fed hike being priced in by the market over a 1m period. Typically, EM FX had negative returns over those periods, although there were some which did not conform to this, such as in March 2016 when EM was going through a cyclical recovery from the lows, and in January 2018.

Three Fed hikes are currently priced in for the next 12 months, and our economists see a likely revision to the Fed dot plot at the March FOMC meeting to indicate four hikes this year. This could add some short-term pressure to EM FX in the run-up to the meeting.

Trading tips:

We are neutral EM FX amid a more balanced short-term risk outlook

EMEA FX: We are MW in EMEA EMFX emphasizing RV plays. In CEE, we now have the highest conviction on our tactical short EURHUF trade added last week. Our conviction on short USDPLN has dropped, but we still believe the direction will be lower for the currency.

EM Asia FX: Neutral in the GBI-EM Model Portfolio but outright longs in SGD, KRW, and TWD, as EM Asia FX strength can play a part in mitigating trade tensions over the medium term.

Latin America FX: Maintain long JPYMXN and long USDCLP. Keep OW BRL and ARS, and UW MXN on medium-term considerations and UW PEN as a hedge.

In a standard carry trade, one takes advantage of a positive interest rate differential between two currencies. This position tends to perform in an environment of depressed volatility since the limited FX risk preserves the yield. However, the long high-yielding currency is almost always pretty volatile when it falls (think of emerging currencies), so the incremental carry profit can be destroyed in a wink if market sentiment deteriorates.

Sell 1Yx1Y USDTRY FVA vs buy 1Y ATM call.

Buy USDTRY call (4.00) and EURTRY call (4.83) (equal weighted USD notional).

FxWirePro launches Absolute Return Managed Program. For more details, visit: