‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data

In contrast to most other currencies, Sterling has hardly benefited from the improved market sentiment in recent weeks. The British currency was only able to gain little ground against the safe haven currencies, the Japanese yen, Swiss franc and the US dollar. But even that can be attributed more to a pronounced weakness of these currencies rather than to a stronger pound.

Several factors have recently taken their toll on the British currency:

- The UK has become the corona hotspot within Europe, which raised doubts about the government's ability to effectively contain the virus.

- The Bank of England has signalled further stimulus measures in view of the corona-induced economic slump.

- The risk of a no-deal Brexit at the end of this year has yet again increased significantly after the negotiations between the EU and the UK on a trade agreement appear to have reached an impasse.

These trios reinforces the potential weakness of the sterling in the days to come. Given that the UK and EU should have a strong interest in the conclusion of a free trade agreement, given the already difficult economic situation caused by the corona crisis, our economists are confident that an agreement on an extension of the talks in the second half of the year remains possible. Nevertheless, they also believe that the probability of a no-deal Brexit has increased significantly. For this reason we are forecasting a weaker pound in the short term and only a very moderate recovery later in the year. In fact, there is a high risk that the pound will suffer much more severe setbacks in the meantime than our forecasts suggest due to rising Brexit risks, hence, we are already short in GBPUSD via optionality.

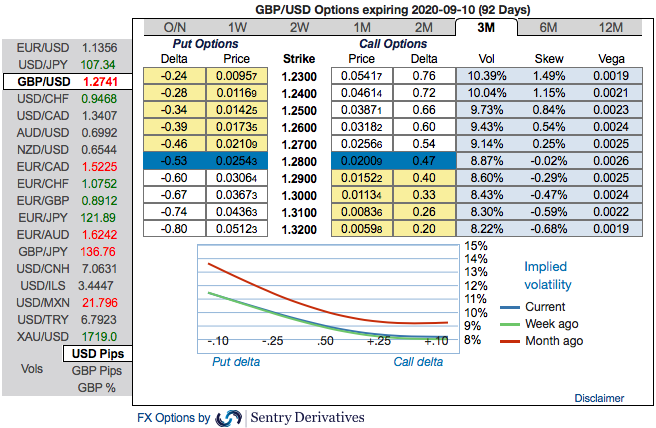

The rationale: GBP will likely take its directional cue from the read-through to BoE’s rate cut whereas the size of the move will be augmented or moderated by the government’s broader policy platform, and most importantly, all these underlying news are factored-in GBP’s FX options market.

You could observe 3m GBP skews that has stretched towards negative territory, hedgers have shown interests for bearish risks as you could see more bids for OTM Put strikes up to 1.23.

To substantiate the downside risk sentiment, fresh negative bids of risk reversal numbers have still been signalling bearish hedging sentiments in the long run. Accordingly, we advocate the diagonal options strategy on both hedging and trading grounds.

Though the underlying spot FX is showing some resistance to the prevailing bearish streaks, these rallies seem to be momentary. Hence, this is right time to write deep OTM put options.

Execution of strategy (Debit Put Spread): Capitalizing on the above factors, it is prudent to deploy diagonal options strategy by adding short sterling via a limited loss tail hedge: Stay short a 2M/2W GBPUSD put spread (1.22/1.2850).

Alternatively, activate shorts in GBPUSD futures contracts of July’20 deliveries with an objective of arresting potential slumps. Courtesy: Sentry, Saxo & Commerzbank