Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

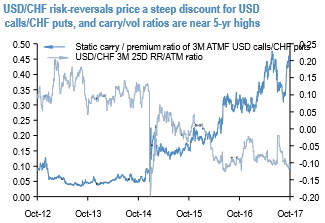

Owning USD calls/CHF puts or USDCHF risk reversals as long USD plays:

Unwind long EURCHF outright and rotate into long USDCHF via a risk reversal, which in conjunction with a pre-existing spot long in USDJPY, positions the portfolio for an ongoing improvement in the US economy.

Rotate long EURCHF into long USDCHF via risk reversal; keep EURUSD call spread, the much-awaited ECB meeting was modestly dovish and with it, Draghi was able to deliver euro weakening alongside a QE “taper” announcement for the second time in a year.

It is stated that USDCHF is one of the only two USD pairs (the other being USDJPY) where owning USD calls has been profitable on a delta-hedged basis since they earn smile theta along a risk-reversal that is bid for USD puts to reflect a premium for a 2015 franc de-peg-like SNB tail event.

In addition, long USDCHF directionally is a positive carry proposition, hence risk-reversals without delta-hedges lean long USD while earning both time decay and forward points.

The RV edge is that risk reversals are depressed via-a-vis ATM vols, which are themselves historically cheap relative to carry in forwards (refer above chart).

A 15’Dec17 (post-December FOMC) 1.01 / 0.98 risk-reversal costs 15bp premium (spot ref. 1.0008), has a very decent spot-to-strike distance ratio of the call and put legs of 1:2.5 and suffers negligible bleed till the final two weeks of its life.