U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Consolidation has proved to be the order of the last twenty-four hours, as equities across Europe, US (yesterday) and Asia rallied following reports that China is to send a delegation to discuss trade with the US. Markets will still be sensitive to geopolitical developments, but successive subdued sessions (in terms of both trade tensions easing and emerging market currency volatility falling) may see attention shift elsewhere.

One factor that may move back into the middle of the market’s line of sight is Brexit. Negotiations between the UK and EU resumed yesterday, following comments earlier in the week from Foreign Secretary Jeremy Hunt that ‘no deal’ risks were rising. There were few headlines yesterday, but according to Bloomberg, the EU’s chief negotiator Michel Barnier may hold a press conference today.

GBP vols and risk-reversals are relatively low for a ‘no deal’ Brexit outcome that has begun to be discussed in UK policy circles.

We discuss a slew of bearish GBP hedges, including deep OTM GBP put/USD call digital options, GBPCHF – USDCHF vanilla put switches and (GBPUSD, USDCHF) dual digital options.

The lingering sentiments around the likelihood of ‘no deal’ Brexit have ratcheted higher of late, most recently following International Trade Secretary Liam Fox’s pegging the odds of such a scenario at 60% in an interview.

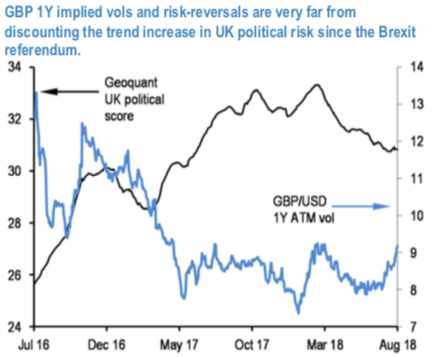

One could argue that GBP vols and risk-reversals have not kept pace with the trend increase in political risks in the UK since the Brexit referendum. 1stchart exhibits a new-age index of political risks scored by Geoquant based on a mix of structural country risk metrics and higher frequency formal and social media data (GEOQUKPR Index(go)); its lack of directional correlation with option price based measures of sterling risk suggests that an unpleasant surprise could be in store for GBP options should markets focus more squarely on the no deal scenario.

Considering 1.20 on GBPUSD to be the hard Brexit threshold – not unreasonable since 1.20 is the spot low in the aftermath of the Leave vote in 2016 – pricing on 1Y 1.20 strike GBP put/USD call digital options of 15.7% of USD notional (mid) at current market (spot reference: 1.2713 levels) strikes us as being on the low side, on net indicating that option markets assign more than 50% additional probability to a benign resolution to UK/EU.

A straightforward application of the digital option pricing exercise above is to own deep OTM GBP put/USD call digital options. 1Y 10% TV GBPUSD put digitals pricing ticked higher but still trades only a tad from multi-year lows in premium, as evidenced by the spot-to- strike distances of such options in (refer 2ndchart). Cost-of-carry/rate of premium decay are unavoidable real-world considerations, and on this front, digitals/put spreads offer greater staying power in the process that is likely to be the erosion of the pound’s value in coming months. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly GBP spot index is displaying shy above -51 levels (bearish), while hourly USD spot index was at -27 (bearish) while articulating (at 09:08 GMT). For more details on the index, please refer below weblink: