UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields

As per last weekly reporting, European high yield funds registered an outflow of €771mm (1.3% of AUM) for the week ending 22 November.

There was a €143mm (2.1% of AUM) net outflow for ETFs and a €53mm (0.6% of AUM) net outflow for short duration funds.

Last week’s fund outflow of €806mm (1.3% of AUM) is revised to an outflow of €829mm (1.4% of AUM).

Let’s now move onto the core area, EUR longs are within 4% of their three-year highs. Meanwhile, the 10- year Treasury/Bund spread remains within a whisker of 200bp, a level it broke through a year ago for the first time since 1989.

These are the two obstacles euro bulls need to get through and even if the euro continues to unwind undervaluation with the help of strong economic data and now, optimism that a coalition government can be formed in Germany, it will inevitably be heavy going.

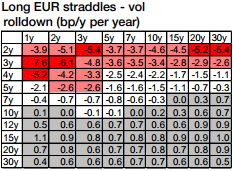

Long positions in EUR bottom-right vega benefit from a positive vol rolldown (refer above graph). They are hence attractive as strategic vol longs.

For instance, the vol rolldown finances roughly 15% of theta in a long 7y30y straddle position and almost 60% of theta in a long 15y30y, making the overall roll down much less penalizing than for the 5y5y benchmark point (refer above graphs).

For the 7y30y, theta cost is completely financed if the 7y30y vol increases in one year’s time by 4.5bp/y (i.e. 0.28bp/d), i.e. moves back to levels seen in 1H’2017. The corresponding breakeven move for the 15y30y vol is only 1.7bp/y (0.11bp/d). Courtesy: SG