How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch

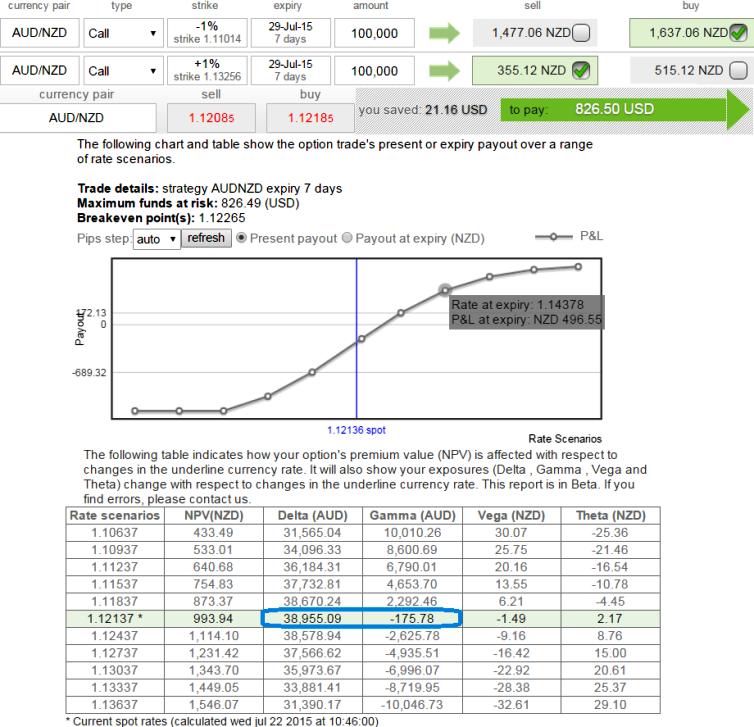

We've been formulating a lot of call spreads on highly volatile currency pairs (AUD/NZD is the one among the pool) and have been drawing up some customized strategies by using P&L tools and techniques to look at the option Greeks.

While doing so it seems like the FX option of this APAC pairs have tons of Gamma. It might be puzzling because on one hand it seems some of these options are highly volatile than any other APAC currency pairs but a tiny shift in the underlying exchange rate would cause instant disaster. This can be arrested by devoting little time on ascertaining an accurate gamma.

As you can observe from the diagrammatic representation, we've constructed call spread by considering gamma closer to zero which would neutralize the implied volatility adverse impact on option prices and this position remains quite firm to achieve our hedging objectives, because we know gamma represents the change in delta, we have healthier delta at 0.38.

This results in desired hedging objective irrespective implied volatility disruptions as we've OTM shorts on side and prevailing bull run will be taken by In-The-Money calls.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirepPro: AUDNZD volatility optimizer through gamma spreads

Wednesday, July 22, 2015 5:49 AM UTC

Editor's Picks

- Market Data

Most Popular