IEA Warns China Rare Earth Export Curbs Could Threaten $6.5 Trillion in Global Production

IEA Warns China Rare Earth Export Curbs Could Threaten $6.5 Trillion in Global Production  Asian Currencies Hold Steady as Middle East Tensions Offset Weaker US Dollar

Asian Currencies Hold Steady as Middle East Tensions Offset Weaker US Dollar  Asian Stocks Rise as Softer U.S. Inflation Boosts Sentiment Despite Middle East Tensions

Asian Stocks Rise as Softer U.S. Inflation Boosts Sentiment Despite Middle East Tensions  China Home Prices Fall Again in June Despite Slower Pace of Decline

China Home Prices Fall Again in June Despite Slower Pace of Decline  Gold Prices Slip as Oil Rally Fuels Inflation Fears, Strengthens Dollar

Gold Prices Slip as Oil Rally Fuels Inflation Fears, Strengthens Dollar  China Q2 2026 GDP Misses Forecast as Weak Domestic Demand Offsets Export Strength

China Q2 2026 GDP Misses Forecast as Weak Domestic Demand Offsets Export Strength  Oil Prices Rise as U.S. Strikes on Iran Raise Strait of Hormuz Supply Fears

Oil Prices Rise as U.S. Strikes on Iran Raise Strait of Hormuz Supply Fears  AI Chip Stocks Face Valuation Pressure as Investors Shift Toward Big Tech and Software

AI Chip Stocks Face Valuation Pressure as Investors Shift Toward Big Tech and Software

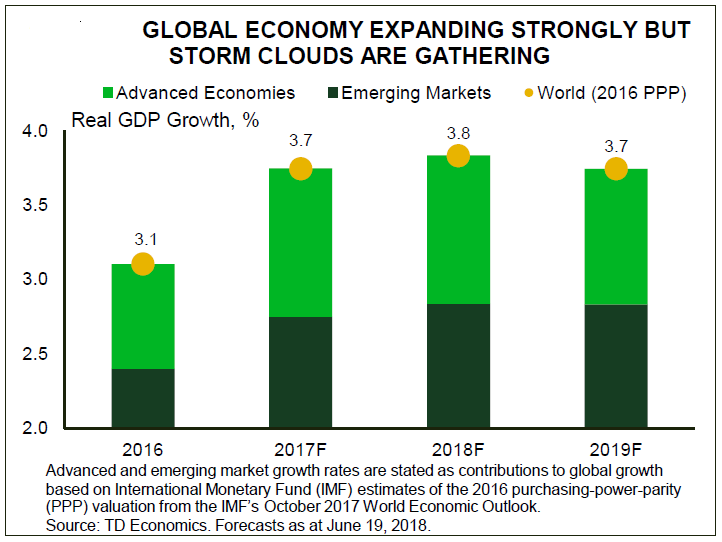

Global growth is expected to run at a robust 3.8 percent this year, similar to last year. However, this steady performance hides a weaker-than-expected start in the Euro Area and the UK, which can be partly chalked up to temporary factors, according to a recent research report from TD Economics.

Fortunately, a recovery from the first quarter stumble appears underway, with both regions expected to benefit from moderately above-trend growth over the next couple of years. It’s already becoming clear that the real standout performer for 2018 is going to be the U.S., which is tracking a 3.0 percent pace. The U.S. is widening its lead on other G7 economies this year, leading to less synchronous growth among the major economies relative to 2017.

Price pressures have also been building unevenly, with core inflation measures already near the central bank targets for the U.S. and Canada. In contrast, underlying wage and price pressures in Europe, the UK, and Japan remain relatively subdued, providing little incentive for a knee-jerk removal of past emergency stimulus.

Further the U.S. dollar rally in the past few months is a reflection of this divergence theme. This may become more difficult to sustain among the G7 currencies, as second quarter economic data offers investors more confidence. However, emerging markets remain vulnerable, as U.S. assets will remain more attractive from a risk-reward standpoint, the report added.

Within Europe, much of the slowdown earlier this year can be chalked up to weakness in France and the UK. Over the next two years, an average projection of about 2 percent for real GDP happens to land right in between last year’s solid 2.6 percent advance and the Euro Area’s long-run trend rate of about 1.3 percent.

"This means economic slack will continue to diminish, even if it’s at a slower pace than previously expected. This is why the central bank has gained confidence in telegraphing plans to commence a long-awaited tapering of its asset purchase program this year," the report commented.

At this point, G7 central banks are choosing to look-through the near-term challenges to the outlook for growth and inflation. As a result, we anticipate that the Federal Reserve is on track to push its policy rate higher in September, and Canada is likely to proceed with raising rates in July, a final time for 2018. Overseas, the Bank of England has become more patient, as unexpected economic weakness and gradually falling inflation has stayed its hand at least until this August.