Wall Street Slides as U.S.-Iran Tensions Escalate; Tech Stocks Extend Losses in 2026

Wall Street Slides as U.S.-Iran Tensions Escalate; Tech Stocks Extend Losses in 2026  Japan Core Inflation Seen Steady in May Ahead of BOJ Rate Hike

Japan Core Inflation Seen Steady in May Ahead of BOJ Rate Hike  Dollar Stabilizes as Markets Weigh Middle East Ceasefire Prospects and Central Bank Policy Outlook

Dollar Stabilizes as Markets Weigh Middle East Ceasefire Prospects and Central Bank Policy Outlook  US Appeals Court Keeps Trump’s 10% Global Tariff in Effect During Ongoing Legal Battle

US Appeals Court Keeps Trump’s 10% Global Tariff in Effect During Ongoing Legal Battle  Changchun Targets EV Growth as China’s Auto Industry Consolidation Accelerates

Changchun Targets EV Growth as China’s Auto Industry Consolidation Accelerates  Oil Prices Fall as Trump Signals Iran Deal, Reducing Supply Risk Concerns

Oil Prices Fall as Trump Signals Iran Deal, Reducing Supply Risk Concerns  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Japan Producer Prices Surge in May, Strengthening Expectations of BOJ Rate Hike

Japan Producer Prices Surge in May, Strengthening Expectations of BOJ Rate Hike  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  China Inflation Misses Forecast as Consumer Spending Stays Weak, Producer Prices Surge

China Inflation Misses Forecast as Consumer Spending Stays Weak, Producer Prices Surge  Oil Prices Surge Above $93 as Trump Escalates Iran Pressure and Strait of Hormuz Tensions Deepen

Oil Prices Surge Above $93 as Trump Escalates Iran Pressure and Strait of Hormuz Tensions Deepen

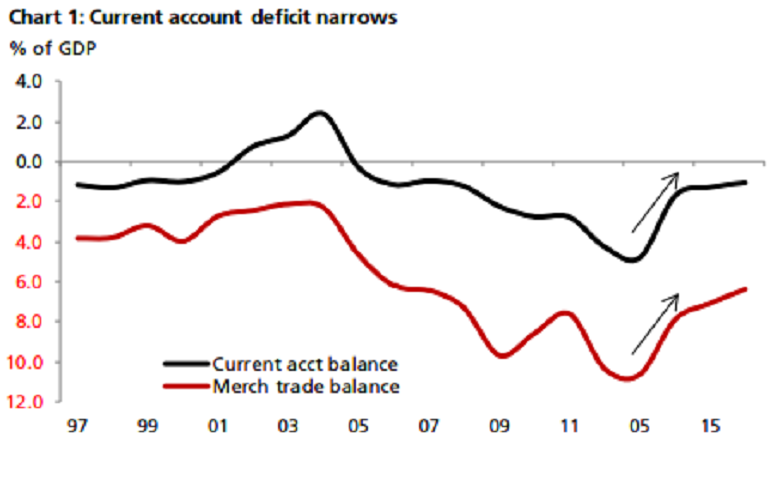

Higher energy prices, coupled with a revival in investment spending pose potential risks to India’s current account deficits, enlarging possibilities of a widened deficit in the near term.

India has run current account deficits (CADs) since the early-1990s, except for a brief period in 2002-04. The deficit averaged 1-2.5 percent of gross domestic product (GDP) over most of the past decade before rising to 4 percent in FY12-13 on the back of a jump in oil imports and gold purchases. It has since fallen back to about 1 percent of GDP and is expected to remain about there for the foreseeable future, DBS reported.

India’s CAD narrowed to 1.7 percent of GDP during the fiscal year 2013-14, from a huge 4.8 percent same period a year ago. A smaller merchandise trade deficit, owing to fall in gold purchases led to the decline. The sharp fall in demand for the yellow metal was engineered through a host of trade and administrative curbs, leading to a sharp 70 percent dive in the metal’s imports in FY13-14. Global commodity prices were also softening, helping cap oil imports.

At the present scenario, the current account has largely benefited from a fall in imports rather than greater exports. The sharp drop in crude prices cut the oil import bill by one-third, while subdued investment demand kept a lid on non-gold non-oil purchases. The latter fell 9.0 percent during Apr-Jul 2016 compared to -4.0 percent during FY15-16.

Amongst invisibles, service receipts and private transfers and/or remittances are also showing signs of strain. Thus the current improvement in the current account is not as favorable as the one in 2002-04. Against this backdrop, the CAD should narrow to 0.8-0.9 percent of GDP from 1.1 percent in FY15-16. A stronger current account balance would be at risk if crude prices hit above USD 60/bbl this year, DBS reported.

At the same time, a pickup in investment could also lift imports, putting renewed pressure on the current account. If these risks materialize, a return to the long-term deficit range of 1.5-2.0 percent of GDP would likely follow. While the size of the current account is important, how it is financed is equally imperative.

"Given the government’s move to raise limits/ relax sector-specific regulations for FDI, undertake reforms to improve the ease of doing business and efforts to streamline the investment process, we expect foreign investment flows to improve in the coming years," DBS commented in its latest research report.