Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

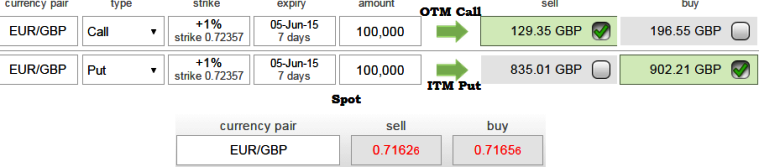

Here we assumed the portfolio contains the same expiration for calculation purpose (it actually has to be near month on call shorting & far month on put) with two different currency derivatives instruments of same underlying currency then they must have the same present value.

Else, arbitrager can go long on the undervalued portfolio and short the overvalued portfolio to make a risk free profit on expiration day.

Hence, taking into account the need to calculate the present value of the cash component using a suitable risk-free interest rate, we have calculated and illustrated the Put call parity of EUR/GBP collar:

C = S + p - Xe-r (T- t)

= 0.7162 + 902.21 - Euler (0.7235*2.71828) - 0.02*(7)

= -901.1

P = c - S + Xe-r (T- t)

= 129.35 - 0.7162 + Euler (0.7235*2.71828) - 0.02*(7)

= 126.8071

Where,

S = Current Exchange Rate

X = Exercise price (strike) of option

C = Call Value

P = Put price

e = Euler's constant - approximately 2.71828 (exponential function on a financial calculator)

r = continuously compounded risk free interest rate = assumed at 2%

T-t = term to expiration measured in years

T = Expiration date

t = Current value date

Note: Before jumping into a conclusion of above calculations, one has to be mindful of how the supply and demand impacts option prices and how all option values (at all the available strikes and expirations) on the same underlying security are related.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Put call parity of EUR/GBP collar

Friday, May 29, 2015 9:09 AM UTC

Editor's Picks

- Market Data

Most Popular

7