Gold Prices Fall as US-Iran Conflict, Rising Oil Prices Fuel Fed Rate Concerns

Gold Prices Fall as US-Iran Conflict, Rising Oil Prices Fuel Fed Rate Concerns  Australia Consumer Sentiment Rises in July as Fuel Price Relief Lifts Confidence

Australia Consumer Sentiment Rises in July as Fuel Price Relief Lifts Confidence  Dollar Slides as Softer US Inflation Dims Fed Rate Hike Expectations

Dollar Slides as Softer US Inflation Dims Fed Rate Hike Expectations  Asian Stocks Rally as Cooling U.S. Inflation Boosts Fed Rate Cut Hopes

Asian Stocks Rally as Cooling U.S. Inflation Boosts Fed Rate Cut Hopes  Asian Stocks Rise as Softer U.S. Inflation Boosts Sentiment Despite Middle East Tensions

Asian Stocks Rise as Softer U.S. Inflation Boosts Sentiment Despite Middle East Tensions  US Inflation Expected to Ease in June, but Fed Rate Hike Risks Persist Amid Middle East Tensions

US Inflation Expected to Ease in June, but Fed Rate Hike Risks Persist Amid Middle East Tensions  Oil Prices Climb as Trump Escalates Iran Pressure, Strait of Hormuz Risks Grow

Oil Prices Climb as Trump Escalates Iran Pressure, Strait of Hormuz Risks Grow  Dollar Rises as Middle East Conflict Fuels Inflation and Rate Hike Fears

Dollar Rises as Middle East Conflict Fuels Inflation and Rate Hike Fears  Oil Prices Surge as U.S.-Iran Conflict Escalates and Strait of Hormuz Risks Grow

Oil Prices Surge as U.S.-Iran Conflict Escalates and Strait of Hormuz Risks Grow

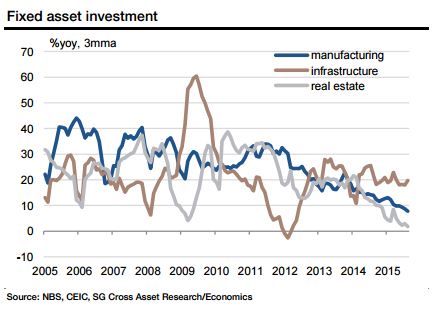

Fixed asset investment (FAI) surprisingly weakened to 9.2% yoy in August, the slowest in a decade. Manufacturing investment growth only ticked up fractionally, despite a positive base effect. Mining investment recorded a sharper decline of 8.2% yoy in August after dropping 1.7% yoy in the previous month. Most worryingly, property investment fell into contraction again from 2.8% yoy in July to -1.2% yoy in August. New starts growth improved slightly in yoy terms, albeit entirely owing to a positive base effect. Housing sales growth remained fairly decent for the fifth month, but this series seems to have lost some of its predictive power for housing construction.

Industrial production (IP) was another big disappointment. Its growth ticked up by a paltry 0.1ppt from the surprisingly slow pace of 6% yoy in July to 6.1% yoy in August, in spite of a strong positive base effect. More than four-tenth of the sectors saw growth weakening in August. Even the statistical bureau commented that the recovery was not so solid and that downward pressures on growth continued to be relatively sizable amid weak demand. Nominal retail sales printed above expectations, growing 10.8%yoy in August (vs. 10.5% in July). However, real retail sales growth remained unchanged. That said, a bright spot is that durable goods consumption strengthened, with acceleration in sales of automobiles and household goods.

All the headline disappointment occurred despite the clear presence of a stronger fiscal push. On-budget spending went from strength to strength, accelerating from 27.1% yoy in July to 28.4% yoy in August. More importantly, infrastructure investment growth jumped from 15.8 yoy in July to 21% yoy in August, on the back of another strong bank lending expansion.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Recovery is still missing for China

Monday, September 14, 2015 1:47 AM UTC

Editor's Picks

- Market Data

Most Popular