Apple Intelligence China Approval Lifts Alibaba and Baidu Shares

Apple Intelligence China Approval Lifts Alibaba and Baidu Shares  Nvidia Partners With Fanuc and Yaskawa to Accelerate AI Robotics in Japan

Nvidia Partners With Fanuc and Yaskawa to Accelerate AI Robotics in Japan  Stripe, Advent Offer $53 Billion Deal to Acquire PayPal: Reuters

Stripe, Advent Offer $53 Billion Deal to Acquire PayPal: Reuters  Stripe, Advent Offer Over $53 Billion to Acquire PayPal in Major Fintech Deal

Stripe, Advent Offer Over $53 Billion to Acquire PayPal in Major Fintech Deal  Rio Tinto Reports Strong Q2 Iron Ore Sales, Maintains 2026 Production Outlook

Rio Tinto Reports Strong Q2 Iron Ore Sales, Maintains 2026 Production Outlook  SK Hynix Stock Soars as AI Memory Demand Outlook Fuels Chip Rally

SK Hynix Stock Soars as AI Memory Demand Outlook Fuels Chip Rally  NY Times Challenges Trump Administration Subpoenas Over Air Force One Report

NY Times Challenges Trump Administration Subpoenas Over Air Force One Report  Richemont Q1 Sales Beat Forecast as Cartier Demand Drives Strong Growth

Richemont Q1 Sales Beat Forecast as Cartier Demand Drives Strong Growth  Sodexo Unveils Shift & Grow 2030 Strategy, Targets Over 5% Revenue Growth by Fiscal 2030

Sodexo Unveils Shift & Grow 2030 Strategy, Targets Over 5% Revenue Growth by Fiscal 2030  Eli Lilly Eyes AtaiBeckley Acquisition to Expand Psychedelic Mental Health Pipeline

Eli Lilly Eyes AtaiBeckley Acquisition to Expand Psychedelic Mental Health Pipeline  Jamie Dimon Warns Anthropic's Mythos AI Poses National Security Risks

Jamie Dimon Warns Anthropic's Mythos AI Poses National Security Risks  xAI Sues Man for Allegedly Using Grok to Generate AI Child Abuse Deepfakes

xAI Sues Man for Allegedly Using Grok to Generate AI Child Abuse Deepfakes  Hyundai Takes Full Control of Boston Dynamics to Accelerate Humanoid Robot and AI Strategy

Hyundai Takes Full Control of Boston Dynamics to Accelerate Humanoid Robot and AI Strategy  Uber to Acquire Delivery Hero in $14.8 Billion Deal to Expand Global Food Delivery Business

Uber to Acquire Delivery Hero in $14.8 Billion Deal to Expand Global Food Delivery Business  DBS Targets S$1 Trillion Wealth AUM by 2030 Amid Asia Wealth Boom

DBS Targets S$1 Trillion Wealth AUM by 2030 Amid Asia Wealth Boom  DeepSeek Eyes China IPO as AI Startup Seeks $71 Billion Valuation in New Funding Round

DeepSeek Eyes China IPO as AI Startup Seeks $71 Billion Valuation in New Funding Round  Volkswagen Launches €28,000 ID. Cross EV as Europe’s Electric Vehicle Demand Accelerates

Volkswagen Launches €28,000 ID. Cross EV as Europe’s Electric Vehicle Demand Accelerates

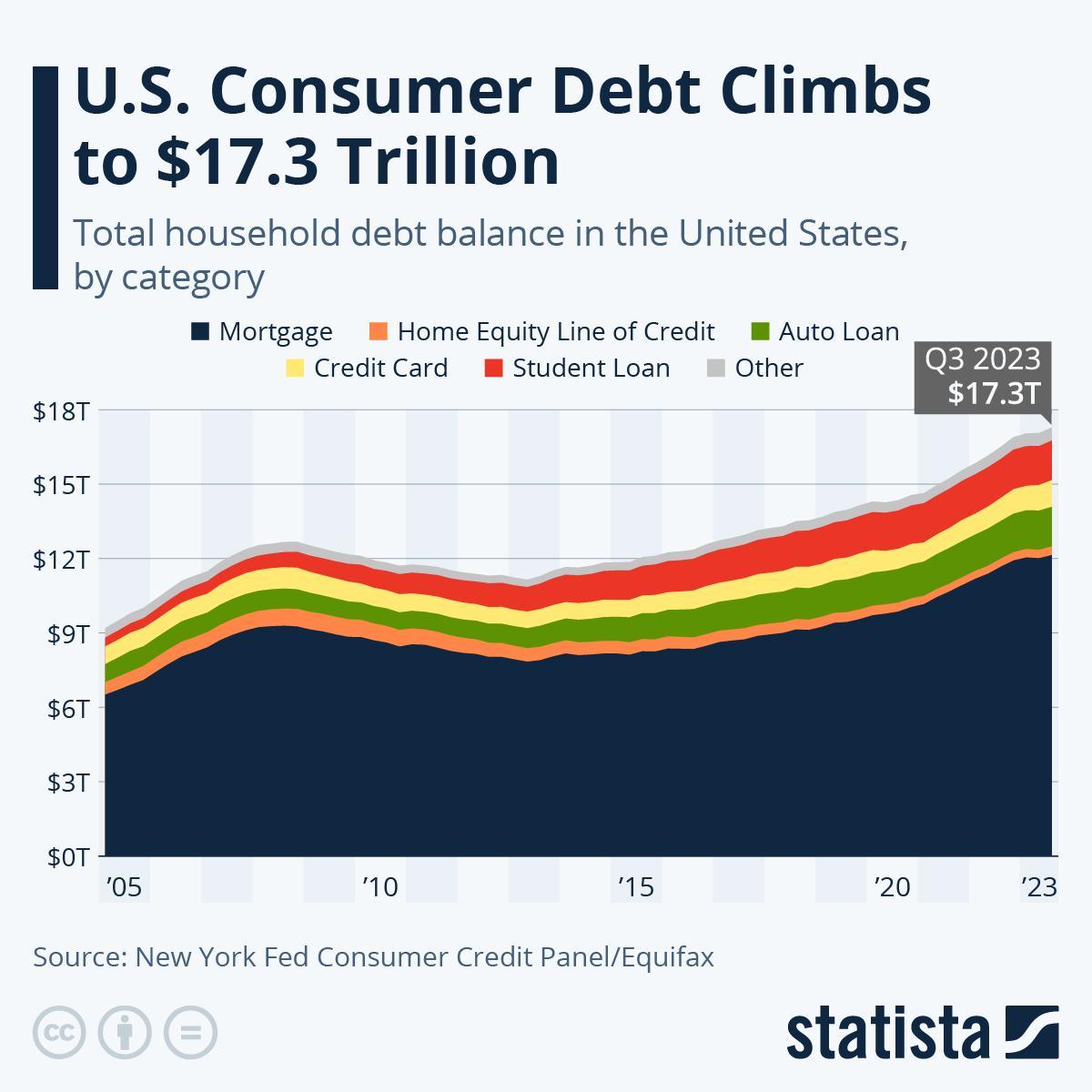

Consumer debt is increasing, and quite frankly, it's getting a little hard to avoid. From credit cards to student loans, people are borrowing more than ever. Understanding what this surge might mean for our wallets and the broader economic landscape is critical in today's fast-paced economy. So let's start with the trends, what's driving them, and what it might mean for you and the whole economy.

Current Condition of Consumer Debt

First, let's get into some numbers: Consumer debt has soared recently, reaching record highs in many categories. As of this year, Americans owe multiple trillions of dollars. Credit card debt has surged significantly, while student loans and auto loans also add to the hefty total. Looking at the data, it is obvious we're in a new era of borrowing.

But it's not just a blanket increase; there are some interesting trends that pop up when broken down by demographics. Younger generations, millennials and Gen Z in particular, are racking up debt in ways we haven't seen before. Meanwhile, for various reasons, including costlier healthcare, the older generation feels the pinch as well. This demographic shift uncovers an elaborate picture, not just who's borrowing, but also why.

Factors Contributing to Increased Consumer Debt

So, what's feeding this explosion? Several reasons take the forefront.

First of all, let's talk about the economy: inflation has become a household word lately, and with rising prices on everything from groceries to gas, many find themselves reaching for credit cards just to make ends meet. Besides this, interest rates are fluctuating. Anytime the cost of borrowing goes up, everything from home loans to credit card interest becomes harder for consumers to pay back.

On the other side of the coin is consumer behavior. Online shopping and digital payments, it's never been easier to spend money. It's just too tempting to swipe that card or hit "buy now" without considering some of the long-term implications. Consumers are all too often relying on credit as if it's a quick fix for expenses today, when in reality, it can build into bigger problems further down the line.

But the pandemic flipped all that on its head, shall we say. COVID-19 changed the world in so many ways. Those government stimulus checks helped in the short term but created a false sense of security, making people almost comfortable taking on more debt. It’s quite the ride these days with much uncertainty, especially in industries facing huge amounts of unpredictability.

What does this all add up to? Well, for one thing, rising consumer debt hits the economy big time. The more people owe, the more it can suppress spending and slow economic growth. If people are paying off debt instead of buying new cars or eating out, the economy suffers.

On a personal level, larger amounts of debt can be seriously stressful. Juggling monthly payments leads to anxiety, a less-than-ideal mental state for anyone. Also, it affects credit scores. A poor credit score drives away options related to buying a home or securing a loan in the future.

There's also the risk of a ripple effect on policy. The larger consumer debt becomes, the more the temptation for lawmakers to take action will grow. We might see discussions of debt relief or regulations to help consumers better manage their finances.

Consumer Strategies

What can you do about it, then? First of all, debt has to be confronted head-on. You have to make a budget, a real game-changer. You'd be surprised how much knowing exactly where your money goes will help you make wiser decisions and prioritize which debts to pay off. Consider the snowball principle for loans: start by paying off the smallest debt. When that's paid off, move on to the next one. It can be satisfying and encourage you to continue.

You may also consider credit card consolidation to make your payments simpler and, often, with lower interest rates. You can combine multiple credit cards into one loan to simplify your monthly payments by focusing on a single balance. Just be sure to read the fine print, because some consolidation options come with fees and/or higher interest rates.

Financial literacy is important. It enables you to understand how credit works and how debt burdens will affect you, so that you can make better choices. There are loads of free resources online, from budgeting applications to financial education programs. Use them!

Conclusion

Today's rise in consumer debt is multifaceted and has wide ramifications. It is not just about the numbers on the page, it is about real life, our economy, and future policies. Let knowledge of this complex landscape keep us informed as we proactively work on our finances. Take a moment to assess where you stand. Understanding where you are can help you make wiser decisions for a healthier financial future.

This is not just about the numbers; it's about making informed decisions that will serve us in the long run. Together, let's take responsibility for our financial futures!

This article does not necessarily reflect the opinions of the editors or management of EconoTimes