China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Trump Unveils $3 Billion U.S. Critical Minerals Push

Trump Unveils $3 Billion U.S. Critical Minerals Push  US Stock Futures Rise as Markets Await July Payrolls Data

US Stock Futures Rise as Markets Await July Payrolls Data  Oil Prices Surge as Iran Hormuz Restrictions Renew Supply Fears

Oil Prices Surge as Iran Hormuz Restrictions Renew Supply Fears  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes

Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes  Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises

Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises  Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue

Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue  Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness

Wall Street Ends Mixed as Dow Hits Record Despite Tech Weakness  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market

As of February 2020, the number of people infected with the coronavirus Covid-19 has surpassed 80,000, with nearly 2,700 deaths. Efforts to contain the outbreak have led to full or partial quarantines of several Chinese provinces and cities, as well as other countries that have been hit. The movement restrictions that have been implemented currently affect 500 million people.

As the human costs in China and other countries continue to rise, the virus is also taking its toll on different industrial sectors – and subdued demand and disrupted supply across industries increase uncertainty over the global economy.

SARS vs. Covid-19

This is the second time in the past 20 years that China is facing contagion coming from the corona virus family. In 2002, SARS epidemic took 800 lives and infected 8,000 people. Although economic impact of SARS was difficult to assess, a 2004 analysis indicates that the global economy experienced a loss of at least 40 billion US dollars in 2003 and a growth slowdown of 1%.

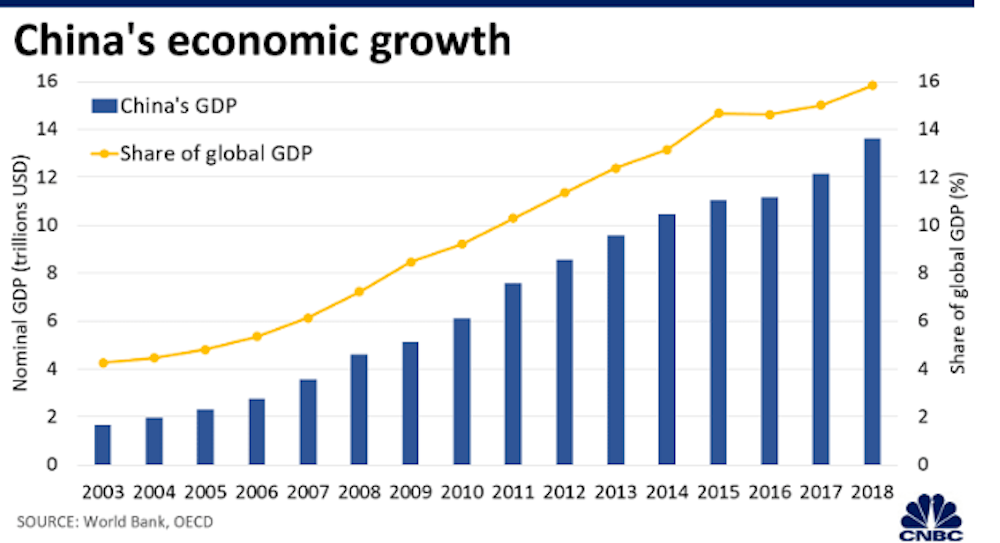

Since early 2000s, China’s economy grown enormously. CNBC

Many things changed since 2003, including the size of the Chinese economy and its position in the world. In the wake of SARS outbreak, China represented slightly over 4% of the global GDP and was the sixth largest economy in the world. Today, it contributes more than 16% of the world’s GDP and is the second economy after that of the United States.

Additionally, the country has traditionally been the biggest source of global growth – in 2019 alone its contribution surpassed 39%.

Manufacturing under distress

Globalisation positioned China at the heart of complex supply chains, as companies worldwide came to depend on supplies from their operations there. As a consequence, factory shutdowns in virus-affected provinces have resulted in shocks across a wide range of industries.

The South Korean carmaker Hyundai was the first firm outside of China to announce that it would halt production in its domestic factories as a result of component shortages. Automobile producers in Europe and the United States have also warned they too will soon start running out of components.

Many global markets are highly dependent on electronic components’ supplies from China. Financial Times

The impact is similar in the technology sector, as China is the leading exporter of electronic components, with nearly 30% of the global export market. Disruptions in deliveries are particularly harmful for countries highly dependent on electronic supplies from China. For example, in 2019 Japan imported more than 45 billion dollars’ worth of Chinese electrical and electronic goods.

Commodity markets face volatility

China is also the largest importer of raw materials, and commodity markets are consequently feeling the impact as well. The International Energy Agency (IEA) expects that global oil demand growth in 2020 will be 30% lower than originally expected – instead of 1.2 million of barrels per day as previously estimated, it will rise only by 825 million barrels per day.

Similarly, the decline of the industrial activity in China has beena shock to the copper market, as the country represents half of global demand. Copper is used in a wide range of industries, including automobiles, mobile phones and domestic appliances. Falling cross-sector sales have resulted in Chinese traders postponing or outright canceling contracts with suppliers from Latin America and Africa, citing “force majeure” clauses – events beyond their control.

Plummeting demand, rising concerns

On the demand side, the impact is already being felt in the travel and tourism industry. The airline sector is expected to have a loss in revenue rising up to 29 billion US dollars this year, as demand for air travel declines for the first time in the last 11 years.

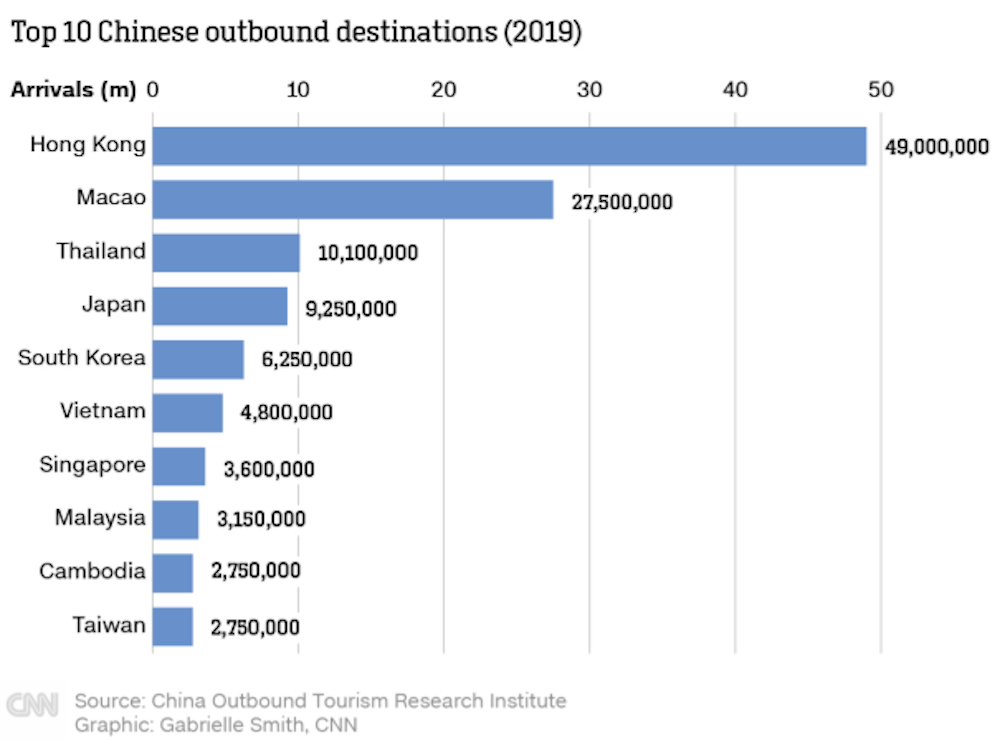

Chinese tourists represent the largest group of outbound global travellers. They favour Asian-Pacific countries – the top three destinations are Hong Kong, Macao and Thailand – and in 2019, Thailand welcomed approximately 10 million visitors from China, representing 30% of its arrivals. Since the outbreak, Thai officials estimate that around 1.3 million visits have been cancelled for February and March alone.

Tourism sector across Asia-pacific region is highly dependent on Chinese tourists. CNN

For the time being, the impact on European tourism is relatively limited. While Paris annually hosts around 800,000 Chinese tourists, this represents only 3% of all tourist visits. However, concerns are raising over the fact that Chinese often travel in groups, with a specific choice of hotels that are now facing vacancies. Similar trends are reported in other European countries such as Germany, Spain and Austria.

A particular passion of Chinese travellers is luxury retail. Since the early 2000s, the country’s shoppers have developed a taste for high-end products and represented for 33% market share for personal luxury goods in 2018, a share that is – or was – projected to rise to 46% by 2025. The industry is now facing its biggest challenge since 2008, as major luxury groups such as Kerring, LVMH and Tiffany become increasingly dependent on rising Chinese demand.

What lies ahead?

What happens next will largely depend on how the Covid-19 crisis evolves. In the best-case scenario, the virus will be contained in the near future or start slowing down in the early spring. People will resume work in China and industrial activity will pick up again. That should bring relief to the Chinese economy and the globe-spanning businesses that depend on it. The lagging demand will likely bounce back relatively quickly, particularly with the help of tailored government measures.

If the virus continues to spread across China, East Asia and other world regions, however, uncertainty and disruption will increase. Movement restrictions would continue and supply chains that are currently temporarily disrupted would decompose entirely, and factory shutdowns would inevitably follow, not just in China but also other markets. Some companies might consider revising their supply chains to find alternatives for China, but experience shows that that’s easier said than done.