Trump Questions USMCA Renewal as Trade Talks Continue

Trump Questions USMCA Renewal as Trade Talks Continue  Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening

Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening  Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns

Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness  Asian Currencies Stabilize as Dollar Holds Near Two-Month High After Fed Hawkish Signal

Asian Currencies Stabilize as Dollar Holds Near Two-Month High After Fed Hawkish Signal  US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge

US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge  Asian Stocks Rally as Japan and South Korea Reach Record Highs on US-Iran Peace Deal

Asian Stocks Rally as Japan and South Korea Reach Record Highs on US-Iran Peace Deal  Asian Currencies Steady as Dollar Holds Firm Ahead of Fed Decision and US-Iran Deal Details

Asian Currencies Steady as Dollar Holds Firm Ahead of Fed Decision and US-Iran Deal Details  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals

Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals

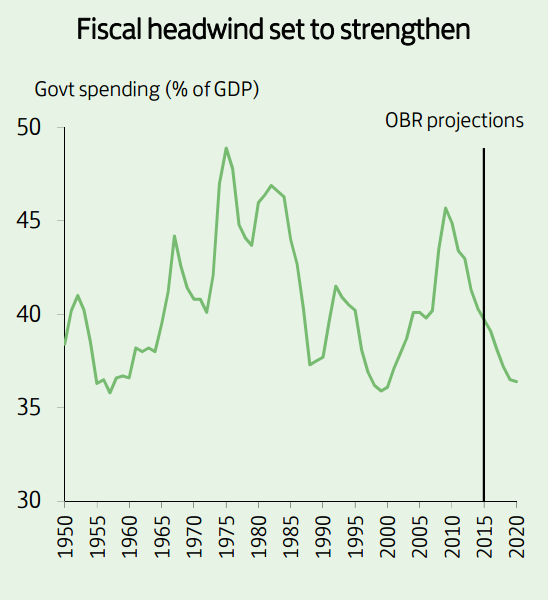

Ongoing fiscal austerity will continue to constrain overall economic growth. While the Chancellor's recent Autumn Statement modestly softened the near-term impact of the cut backs - increasing spending and cutting borrowing relative to the projections in the July Budget - the big picture remains that the bulk of the structural consolidation still lies ahead.

Indeed, the fiscal headwind over the next few years through to 2020-21 is set to be larger than that seen to date since 2010. Latest forecasts also project public spending as a share of GDP dropping to just 36.4% by 2020-21, a low previously only seen briefly in recent history in the late 1950s and late 1990s. The scale of the coming cuts continues to raise doubts about whether they will be achieved. Risks thus remain either of slippage, or of an outsized adverse impact on the economy.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

UK fiscal headwind still strong

Thursday, December 10, 2015 10:01 PM UTC

Editor's Picks

- Market Data

Most Popular