German Auto Suppliers Turn Bearish as Investment and Jobs Shift Overseas

German Auto Suppliers Turn Bearish as Investment and Jobs Shift Overseas  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness  Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention

Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention  German Industry Employment Falls to Lowest Level in a Decade

German Industry Employment Falls to Lowest Level in a Decade  Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns

Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns  Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets

Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets  Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening

Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening

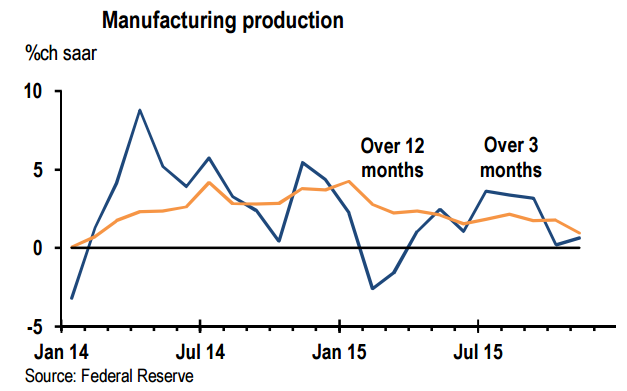

The November IP report confirmed that manufacturing continues to underperform the overall economy. Total manufacturing output was flat in November and non-auto output increased 0.1% samr. This leaves total manufacturing up only 0.8% saar so far in 4Q15 and non-auto manufacturing up 1.1%. These anemic quarterly growth rates are close to the trend in output growth over the first 11 months of the year, 1.1% saar for all manufacturing and 0.6% for non-auto manufacturing.

Moreover, December manufacturing surveys to date point to continued weakness through the end of the year. The PMI had been holding up better than other surveys, but the flash PMI for December dropped to 51.3, its lowest reading since October 2012. The key new orders component dropped to 50.5, its lowest reading since September 2009. Results from the first regional Fed surveys for December were also generally downbeat, in line with the tone of the PMI.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

US manufacturing still struggling

Monday, December 21, 2015 11:39 PM UTC

Editor's Picks

- Market Data

Most Popular