Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough  Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target  Should I take zinc or eat oysters to ward off colds, boost my immune system or improve fertility?

Should I take zinc or eat oysters to ward off colds, boost my immune system or improve fertility?  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.

A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell

Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell

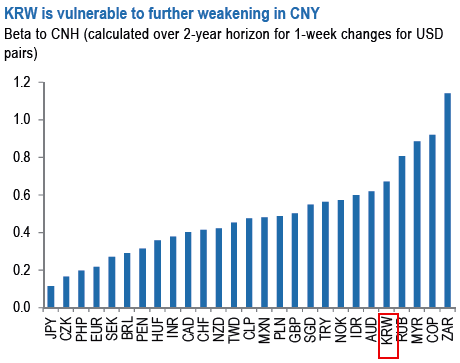

The EM strategies have turned underweight on Asia FX given a combination of higher core yields, the break out of USD/CNY to above 6.70 and multiple idiosyncratic issues.

The capital outflows from China had already picked up before expectations of a Fed hike and despite resilient data.

The additional dynamic of USD strength and expectations of a Fed hike in December suggests that risks to capital flight are skewed to the upside in Q4.

As a result, the expectation is for CNY weakening to accelerate in Q4, with spillover to the rest of the region as well.

KRW is a notable candidate to short given that it has among the highest sensitivity in Asia to CNY weakness (see above chart).

In South Korea, the September exports drop inflated by temporary factors.

The consumer price inflation surprised on the upside.

The BoK left its base rate steady for the fourth straight month at the record low of 1.25 pct at its October meeting, as anticipated.

In addition, the added uncertainty on corporate earnings has the potential to slowdown equity inflows from offshore investors. So, long USDKRW are encouraged at 1135.43 via 3m NDFs.