Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

It seems the tear between the BoJ and the government is getting widening. It is in progress with the BoJ meeting, where the two government representatives urged the BoJ to drop the goal to reach inflation target at the earliest date possible.

We think the BoJ should not focus on introducing further QE which the markets at present broadly expect as do our economists.

The labour market data suggests strength, the company data (new orders) points to improvement in capital investments. The past JPY weakness will support the exports going forward - the lagged effects are at work. Improving current account balance in turn should be positive for the JPY.

And ending with the highlight of the previous few weeks' PM Abe's key economic adviser Hamada stating that USD/JPY would further appropriate on a PPP basis. And indeed the JPY weakening in future seems unlikely. Winds of change retrospectively relative to other currencies as well.

Hence, in coming months we expect Yen getting further strength against dollar.

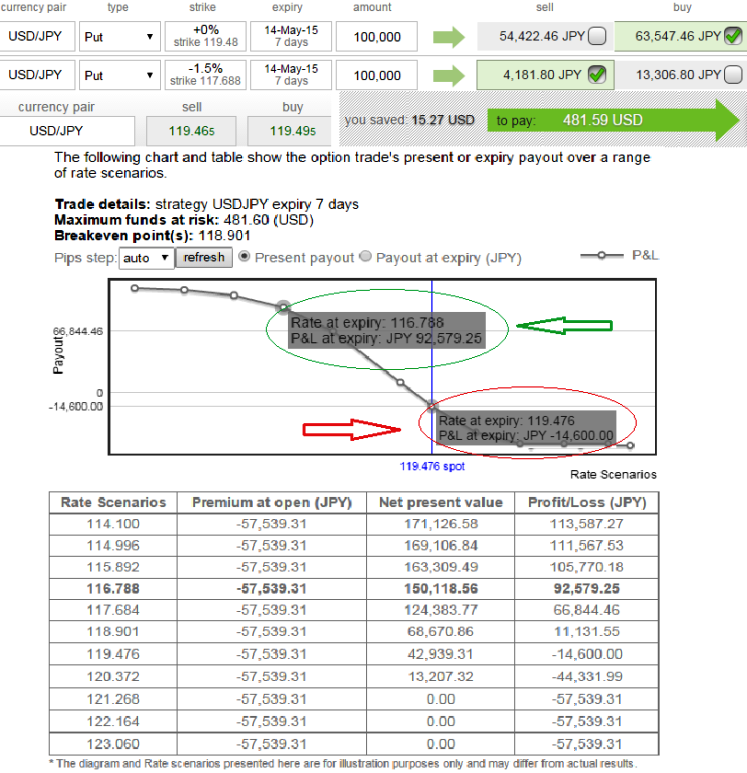

Derivatives advisory:

Option strategy: Bear Put Spread (BPS)

It is a partial hedge strategy which only minimizes the loss if the underlying currency has to move lower but does not cap the loss.

Bear Put Spread shall be used over Protective Put when the premiums on Protective Puts are too costlier.

Bear Put Spread = Protective Put + Sell another Put with lower Strike Price (Out of the Money).

Bear Put Spread reduces the cost of hedge by the premium collected on the Out of the money Put but it comes at the expense of Partial hedge rather than a complete hedge.

The above chart explains how this strategy considering in a scenario evidences the different profitability at different intervals of exchange rates.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Expect stronger Yen, BPS safeguards US traders’ cost of hedging

Thursday, May 7, 2015 7:25 AM UTC

Editor's Picks

- Market Data

Most Popular