Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets

Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets  US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge

US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge  German Auto Suppliers Turn Bearish as Investment and Jobs Shift Overseas

German Auto Suppliers Turn Bearish as Investment and Jobs Shift Overseas  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Italy’s Economy Outpaces Eurozone Peers as Investment Spending Fuels Growth

Italy’s Economy Outpaces Eurozone Peers as Investment Spending Fuels Growth  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Asian Currencies Steady as Dollar Holds Firm Ahead of Fed Decision and US-Iran Deal Details

Asian Currencies Steady as Dollar Holds Firm Ahead of Fed Decision and US-Iran Deal Details  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Canada Imposes 10% Tariff on Canned Vegetable Imports to Protect Domestic Industry

Canada Imposes 10% Tariff on Canned Vegetable Imports to Protect Domestic Industry  Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict

Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict  German Industry Employment Falls to Lowest Level in a Decade

German Industry Employment Falls to Lowest Level in a Decade

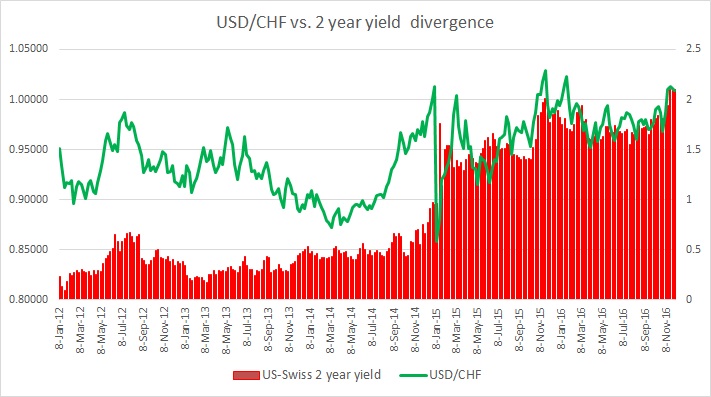

In recent days, Swiss franc’s correlation with the 2-year yield spread (US-Swiss 2 year) has risen to 78 percent and time on time again it shows relatively high positive correlation, as high as 90 percent at times. Just before and after the Brexit referendum in the UK, the 20-day rolling correlation was averaging above 60. Hence, it is vital to keep a watch on the Swiss yields.

Just after the Swiss floor shock in January 2015 when the Swiss National Bank (SNB) removed a floor in EUR/CHF at 1.20 this relation went to negative and stayed there till October with occasional bounces to positive territory. It hasn’t gone much to the negative since.

Unlike the euro or the pound, Swiss franc is considered a safe haven currency; hence the yield relation sometimes gets overlooked.

However, Swiss yields are a must watch as they are the lowest for any government bonds in the world and any shift in that will mark a major turnaround in trend. The above chart explains how the relation between the spread and exchange rate has unfolded since 2012. The recent weakness in the franc can also be attributed to the sudden sharp rise in the yield difference after Republican candidate Donald Trump won the US Presidency. As of now, the yield spread is at 2.01 percent and the franc is currently trading at 1.009 per dollar.