Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Following some rather dull trading days, USD traders had actually hoped for today’s semi-annual hearing of Fed Chair Janet Yellen in front of Congress to bring some life into the exchange rates. But then things happened in rapid succession yesterday - to the dollar’s disadvantage.

The focus of USD investors rests mainly on monetary policy again. Following yesterday’s comments of FOMC board member Lael Brainard a Fed timetable seems to be increasingly emerging that corresponds to the one long since favored by us: the Fed is likely to announce the imminent end of the reinvestments from the QE programme in September.

No clashes with low-intensity jitters continuing through this month as the position shakeout in duration-heavy bond markets play itself out; indeed, the recent FX price action is very much in line with our baseline 2H’17 view of a moderate turn higher in vol. At the same time, however, we are skeptical that the ongoing bond sell-off will morph into a more sinister trigger for risk markets.

That said, these are not placid markets and there are a couple of lessons to be gleaned from the pattern of recent vol returns that can prove useful for defensive option plays:

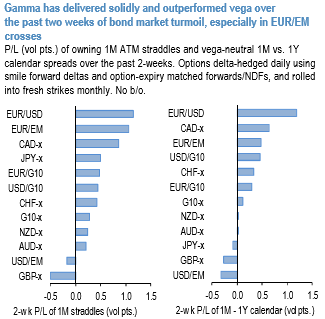

Gamma is performing solidly, and comfortably outpacing vega (refer above chart), which is to be expected when markets go into a pothole with ultra-low levels of frontend vol and steeply upward sloping vol curves. Vol curve flattening was indeed one of our core views for H2, and the upbeat performance of vega-neutral, long gamma calendars supports our conviction in employing them as defensive vehicles.

The currency bloc breakdown of gamma returns in the above chart is divulging. EURUSD and EUR/EM are the best-performing currency pairs, while USD/EM, GBP, and AUD-crosses have been disappointing. In general, owning gamma in USD - pairs and EUR - crosses - the two currencies at the heart of the rate normalization dynamic - appears to be a decent rule of thumb. The underperformance of USD/EM as a bloc is surprising and illustrates the wide dispersion in EM FX behavior.