Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

Any currency option deal may be equivalently valued as either a call or a put using a parity condition that is specific to currency options. We may see that when put-call parity is broken, risk-free arbitrage opportunities may exist.

We’ve considered AUDNZD ATM contracts to exhibit the concept, this condition states that:

Holding a call option to buy 1 unit of NZD for x units of AUD is equal to the holding a put option to sell x units of AUD for 1/x units of NZD.

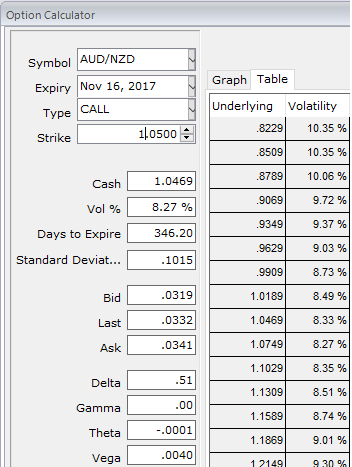

Let’s suppose a foreign trader has purchased NZD ATM Call / AUD ATM Put of 1Y expiry in European vanilla style with a face value of AUD $1 million.

The risk-free rate in AUS is +2.012% (3M prevailing AUS T-bill rate),

The risk-free rate in NZ is 2.070% (3M prevailing NZ T-bill rate),

FX rate volatility is at around 8.27%, and let’s say option expiry would be 1 year.

The spot FX is 1.0469 (Direct quote while articulating) and the strike rate is 1.05 since this is 1y ATM contract.

Consider AUD as the domestic CCY, so the spot must be quoted as the number of units of NZD required to purchase 1AUD.

To value the option as a call, we treat the AUD as the domestic CCY and the NZD as the foreign CCY. The domestic and foreign interest rates are therefore 2.012% and 2.070%, respectively.

Note that once both the spot and strike quotes are converted, the call option is out of the money.

When these parameters are passed to the Garman-Kohlhagen routine, a value of NZD 0.03573 is returned.

This is a per unit value, and since a total of 1 million Aussie dollars underlie the deal, the total premium value is 0.03573 * 1,000,000 = NZD 35,730 (with allowance for rounding).

In order to demonstrate the parity condition, we could also value this deal as a put. In this case, the domestic (foreign) CCY is the AUD (NZD), the domestic (foreign) interest rate is 2.070, the spot rate is 1.0469 and the strike rate is 1.05.

With these inputs, the model returns a value per unit FX of AUD 0.320 and the total value of the premium on the deal is AUD 32,000. This amount is equivalent to the NZD premium computed above when it is converted to NZD at the spot rate of 1.0469.

If the spot FX is expressed in a consistent approach to the strike price, then the computed total premium for the call leg will be the same as the computed total premium for the put leg, assuming both values are expressed in the same currency.