How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

The recent commodity price meltdown and especially the crude's struggle causing the reaction function of firms in the Canadian oil and gas sector proposes that business investment may be even more of a drag on 2016 growth than previously thought.

The Business Outlook Survey by Bank of Canada has been lackluster in Q4 2015 and has amplified this theme, as investment intentions moved to their lowest readings since the 2009 recession. This has prompted the market to price in the increased probability of a rate cut at the January 20 meeting.

Regardless of whether or not the Bank of Canada cuts rates, we believe that the uptrend in USD/CAD will persist. The 1.5000 level now serves as an anchor for the market from a behavioural/sentiment perspective.

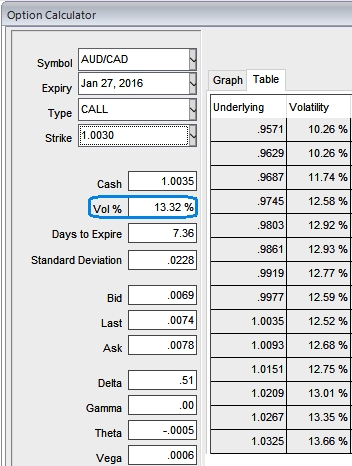

Currency option framework: (AUDCAD Daigonal Condor Spreads)

Our opinion on AUDCAD in Q1 2016 has differently attributed from what we have mentioned above, some uptrend sentiments but we expect range bounded movements in medium to long terms considering the increased volatility (projected a gradual increase in 1m-3m ATM contracts at 10%) and neutral delta risk reversal.

When we had to study and compare this fluctuation of volatility and its comparison with risk reversals of this pair we tend to increase upper limits in the range as a result of increase in the IV.

So to protect the FX portfolio from this fluctuation the below strategy is advisable, the recommendation goes this way, shorting OTM call and buy deep OTM delta calls, simultaneously short ITM call and buy deep ITM delta call options. Prefer as shorter expiries as possible on short side (let's say 4D), 1M expiries on long side as the implied volatility in OTC fades away after the BoC policy actions.

The highest loss for this option strategy is equal to the initial debit taken when entering the trade. It happens when the underlying exchange rate on expiration date is at or below the lowest strike price and also occurs when the pair is at or above the highest strike price of all the options involved.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: CAD seems vulnerable regardless of BoC policy stance - stay hedged via AUD/CAD condor spread on HY vols

Wednesday, January 20, 2016 7:05 AM UTC

Editor's Picks

- Market Data

Most Popular