Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

The Central Bank of Turkey raised its benchmark one-week repo rate by a higher-than-expected 50bps to 8 pct on November 24th and its overnight lending rate by 25 bps to 8.5 pct, while it held its borrowing rate at 7.25 pct.

It was the first policy tightening since January 2014, after the lira fell to a record low amid a slowdown in economic activity.

Consequently, as we urged for the upside potential of USDTRY in our recent posts, the pair’s all-time highs takes off to the new stages, edging towards 3.5 marks. All we could say is that never buck the major trend and the major trend has been the bullish trend but expect interim dips in between for fresh longs.

The Turkish lira weakened sharply in the recent times, with USDTRY surpassing 3.05 range and then to hit fresh highs of 3.4083 levels.

The lira has already lost around 24 pct of its value against the dollar this year on a stronger dollar (from the lows of 2.7891 to the current 3.3408 levels) and concerns over the aftermath of July's failed coup. Inflation was last recorded at 7.2 pct in October, well above central bank's 5 pct targets.

This was definitely in the right direction as a starting point – but it did not work to pacify the lira. This is because the mix of policy measures adopted today showed explicit signs that CBT is having to compromise with government pressure to ease monetary policy; the CB had to cut RRR at the same time that it raised rates.

Hence, question marks linger about whether CBT could go any further if required. We forecast another 50bps rate hike in early 2017 and see USDTRY rising to 3.60 by Q2 2017.

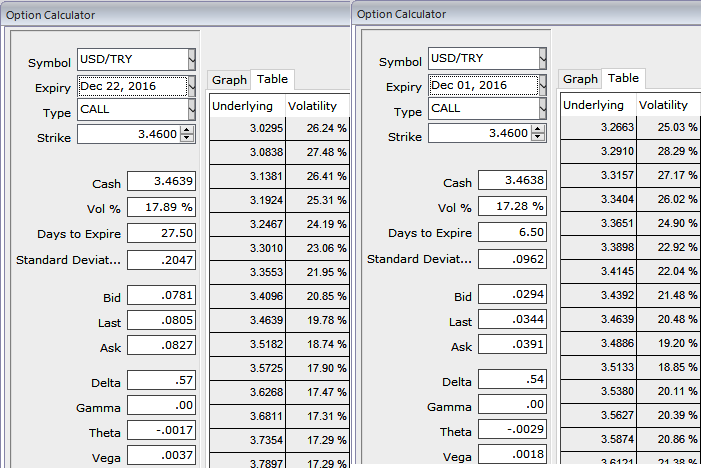

FX Option strategy:

We still uphold the above-advocated FX option spreads as the further upside risks are foreseen and our longs in calls are on pretty well on its functionality, in outright trades, we maintain the longs in USDTRY 1m15d debit call spreads, complementing above aspects and IV shift, the position reduces the hedging cost almost close to 25%.

1m ATM IVs are spiking higher above 17.89%, which is conducive for option holders, Call spreads are preferred over vanilla structures given elevated skew and favorable cost reduction.

Buy USDTRY (3.3580/3.60) call spread with 1m2w at a net debit.

The net delta of the position should be around 48 (3.3580 ITM strike = 78 delta) and selling the upper leg call (OTM strikes) likely to reduce the cost of the ITM call by almost close to 20-25%.