U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

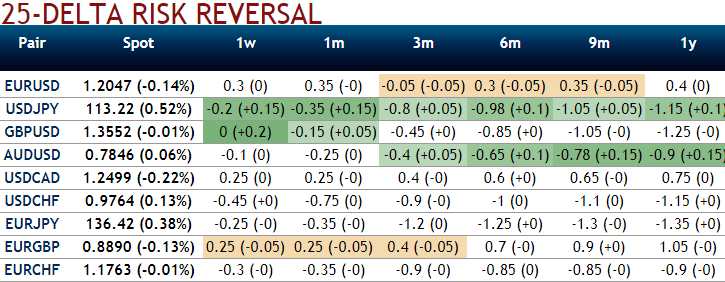

Dollar tantrum is still on despite substantial hurdles cleared in the US tax reform process, and a Fed rate hike. The conviction of broad USD strength through 1Q seems to be shrinking away as the greenback has failed to respond to the recent tax reform developments and disinflation uncertainty is weighing once more, moreover, US Fed remained dovish by not signaling acceleration in hikes for 2018 despite building in assumptions of fiscal stimulus. This implies any 1Q dollar strength might be much narrower and a greater likelihood that the range-bound and idiosyncratically driven conditions for the past month will spill over into 1Q’18.

When the tide and wind are moving in opposite directions, the sea is rough and sailing is hard work. The wind is in the euro’s sails, pushing it higher as the economy grows, the ECB edges away from post-GFC policies and the currency’s undervaluation support it. However, the tide of positioning (long euros) and yield differentials (still heavily in the dollar’s favor) is against the euro. The upshot is that progress from current levels towards ‘fair value’ somewhere closer to EURUSD 1.25, seems to be choppy and sluggish.

Well, all these fundamental developments are factored in EURUSD OTC markets.

Let’s glance at sensitivity tool and risk reversals that indicate no changes in the hedging sentiments in next 1m time and mounting hedging sentiments for bearish risks of the underlying spot FX prices in next 3m-9m timeframes.

This sentiment is substantiated by the positively skewed IVs of 1m/3m tenors that have been signifying the hedgers’ interests of both OTM calls in 1m expiries and well balanced that shows interests in put strikes upto 1.18. Hence, this means that the ATM instruments have likelihood of expiring in-the-money within their respective tenors.

Accordingly, in order to arrest this upside risk that is lingering in short-term trend and the major declining trend, we recommend diagonal debit put options strategy that favors in reducing hedging cost.

Based on this rationale, conservative hedgers can prefer the below strategy:

Diagonal Debit Put Spread = Go long 3M ATM -0.49 delta Put + Short 1m (1%) OTM Put with lower Strike Price with net delta should be at -0.40.

For a net debit bear put spread reduces the cost of trade by the premium collected (on the shorts of OTM put) and keeps option trader to participate in downward moves and any upswings in abrupt.

Moreover, the risk is capped to the extent of initial premium paid, as opposed to unlimited risk when short selling the underlying outright.

However, put options have a limited lifespan. If the underlying FX price does not move below the strike price before the option expiration date, the put option will expire worthless.