Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

The USDTRY is slowly moving back towards the recent highs of 4.0345 level, which could be retested again. As the TRY has depreciated by almost 10% against the dollar compared to the previous year, the currency weakness could push inflation up again and thus exert renewed depreciation pressure on the lira due to the well-known feedback mechanism.

The defensive ploy of using high carry to subsidize the cost-of-carry of long vol is more appropriate to apply to currencies like TRY at the other end of the spectrum, wherein the broader terms, the macro standpoint is bearish. The EMEA analysts note that real yields in Turkey are still too low to sustainably bring down inflation, the current account deficit continues to widen, and the likelihood of comfortably funding the BoP through a repeat of 2017’s heavy portfolio inflows are slim.

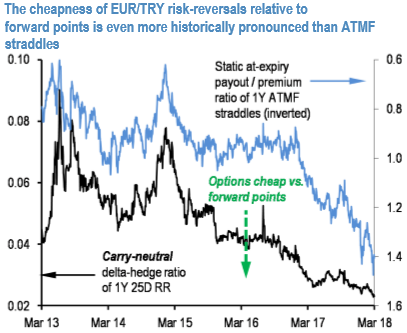

More than outright long vega, bearish TRY views are well expressed through partially delta-hedged risk-reversals, in our view.

While ATM vol is cheap vs. carry, risk-reversals are even cheaper. One measure of a carry-adjusted risk reversal is carry-neutral delta-hedge ratio – the notional of forward delta hedge that needs to be layered atop unit notional/leg of a risk-reversal in order for the static points carry of the forward at expiry to completely offset the net option premium of the risk-reversal.

The lower this ratio, the cheaper the risk-reversal; in extremis, a ratio of zero indicates that the risk-reversal itself is costless and requires no bleed-reducing forward hedge overlay.

The above chart shows that this gauge is historically even more extreme than the corresponding metric for ATMF straddles.

Carry-neutrally delta-hedged risk-reversals are not just skew valuation metrics, but can also function as tradeable constructs for playing defensive directional views. Consider the following as a bearish TRY expression:

Off spot ref. 4.9345 and 3M forward ref. 5.0620, buy €100mio/leg of a EURTRY 3M 5.22 / 4.82 risk-reversal @ 76bp/92bp net premium indic. (vols 12.4/13.1 indic. vs. 10.6 choices) and sell €25mn of EURTRY 3M forward.

The notionals of the option and forward legs are sized such that the static carry on the forward with unchanged spot completely offsets the net riskie premium. The net package has a BS forward delta of €24mn (€49mn of the risk reversal -€25mn of the forward), which is, in theory, “carry-free.”

FxWirePro launches Absolute Return Managed Program. For more details, visit: