US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge

US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge  Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns

Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns  Asian Currencies Stabilize as Dollar Holds Near Two-Month High After Fed Hawkish Signal

Asian Currencies Stabilize as Dollar Holds Near Two-Month High After Fed Hawkish Signal  France Faces Long Road to Economic Rebalancing as Weak Demand and High Rates Weigh, Says Citi

France Faces Long Road to Economic Rebalancing as Weak Demand and High Rates Weigh, Says Citi  Oil Prices Drop as U.S.-Iran Talks Ease Supply Concerns

Oil Prices Drop as U.S.-Iran Talks Ease Supply Concerns  Canada Imposes 10% Tariff on Canned Vegetable Imports to Protect Domestic Industry

Canada Imposes 10% Tariff on Canned Vegetable Imports to Protect Domestic Industry  100+ Global Companies Push Governments to Prioritize Electrification for Economic Growth

100+ Global Companies Push Governments to Prioritize Electrification for Economic Growth  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness  Canada, British Columbia Launch $5 Billion Infrastructure Partnership to Boost Housing, Transit, and Healthcare

Canada, British Columbia Launch $5 Billion Infrastructure Partnership to Boost Housing, Transit, and Healthcare  Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets

Asian Stocks Surge as Oil Prices Fall and Strong US Dollar Weighs on Markets  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Gold Prices Slide as Hawkish Fed and Strong Dollar Weigh on Bullion

Gold Prices Slide as Hawkish Fed and Strong Dollar Weigh on Bullion  Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback

Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback  Trump Says No Hormuz Strait Tolls During 60-Day Iran Ceasefire

Trump Says No Hormuz Strait Tolls During 60-Day Iran Ceasefire  US Stock Futures Recover as Iran Signals Progress in Peace Talks

US Stock Futures Recover as Iran Signals Progress in Peace Talks  Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict

Europe EV Demand Surges as Fuel Prices Rise Amid Iran Conflict  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

The US economy advanced an annualized 1.9 pct on quarter in the three months to December of 2016, lower than a 3.5 pct expansion in the previous period and below market expectations of 2.2 pct, advance estimates showed.

The deceleration in real GDP in the fourth quarter reflected a downturn in exports, an acceleration in imports, a deceleration in PCE, and a downturn in federal government spending that were partly offset by an upturn in residential fixed investment, an acceleration in private inventory investment, an upturn in state and local government spending, and an acceleration in non-residential fixed investment.

Elsewhere the detail is mostly encouraging –

The personal spending added +1.7ppts,

The business investment chipped in with a +0.3ppt addition to growth (the best in nearly 2yrs) and

The housing investment also added +0.4ppts, the highest in a year.

Private domestic demand, a better gauge of growth, came in at a decent 2.8%, broadly in line with the Fed's expectations of moderate growth.

Durable goods orders fell 0.4% in December (vs +2.5% expected), the drop mainly due to a 2.2% decline in transportation orders that defied gains in Boeing orders and vehicle assemblies.

Ex-transportation there was a 0.5% gain alongside solid equipment and shipments data that accounted for a stronger than expected report overall.

Inflation expectations (Michigan Univ.) for 5-10yrs ahead rose from December’s 2.3% record low to 2.6%, while overall consumer sentiment was revised higher.

The U.S. central bank is seen raising borrowing costs later this year given the fiscally expansive policies proposed by Donald Trump, and the new president’s agenda may help to lift wages in 2018, hoisting labor costs, the bank said in a Jan. 25 report.

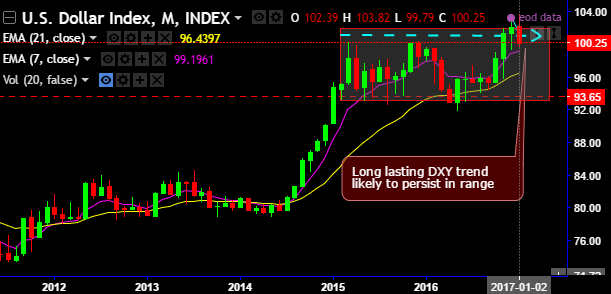

While the dollar index (DXY) seems edgy at this juncture but senses strong support at 100 marks. The dollar index trend has been oscillating between 93 and 103 range since march 2015. To our surprise there seem to be no lingering doubts as to how reliable the news we are being told by the Trump camp are.

The Japanese yen was the major gainer, with USDJPY at around 114.700 levels, while the euro and, to a lesser extent, the pound also rose against the US dollar.