‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes

Asian Stocks Slip as AI Rally Fades, Oil Holds Steady on Iran Peace Deal Hopes  China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade  Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan

Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease

Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Dollar Holds Near Six-Week Low as Yen Loses Momentum Ahead of U.S. Jobs Data

Dollar Holds Near Six-Week Low as Yen Loses Momentum Ahead of U.S. Jobs Data

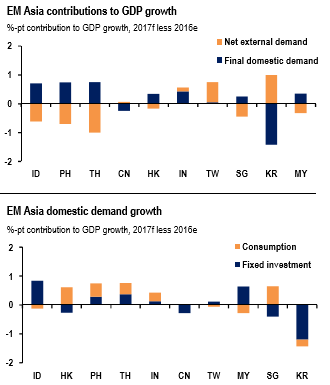

Asia focus: 2017 growth drivers: With GDP growth for the final quarter of 2016 rolling in from around the region. As per the JPM’s projections, EM Asia GDP grew 5.8% in 2016, in line with their expectations at the beginning of last year (refer above nutshell). Looking ahead, the forecasts go another tick down in regional growth to 5.7% in 2017, the second year of sub 6.0% growth since 2001.

The expected slowing in the regional heavyweight China weighs down 2017 EM Asia growth forecasts, as its solid domestic demand conditions in 2016, supported by a robust housing market, likely will soften this year. The recovery in consumption in India, due to the fading impact of demonetization, should partially offset the slowing in China (refer above diagram).

Outside of China and India, domestic demand conditions remain positive this year, except in Korea, where political uncertainty and tight fiscal policy likely will drag on investment growth. A stronger tech cycle likely will contribute more to growth in Korea and Taiwan in 2017 than in 2016. In ASEAN, fiscal spending should keep domestic demand firm, while consumption remains more mixed (refer above diagram).

Our long dollar risk is selective and focused on low yielders (except CNH) and mostly via options.

Stay long USDKRW via 1x2 call spread: Good entry point with 61.8% retracement level from the September low to December high coming in around 1136. 1x2 structure improves max leverage to 9 times from 3 times in a 1x1.

Stay long USDSGD via a one-touch: Worried about French elections and EUR parity? SGD 3m implied vol about 40% cheaper than EUR vol.

Stay long USDCNH via a 1y seagull: Expensive to bet against the CNH. Seagull provides upside exposure that is cheapened significantly by selling expensive 1y vol.

Initiate long USDTWD: Tactical position to fade YTD strength in TWD; could face more formidable support above the May 2015 low (30.39).