European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

Last week, we saw Euro area composite PMI posting a solid gain in October, signaling 1.8% ar GDP growth.

The improvement was broad-based by sector and country and was reinforced by IFO and EC surveys.

Last week’s Q3’16 flash GDP prints an unchanged 0.3% QoQ, SAAR growth, with modest downside risks, while Japan managed to produce an upbeat numbers of 0.5% versus forecasts of 0.2% and previous 0.2%.

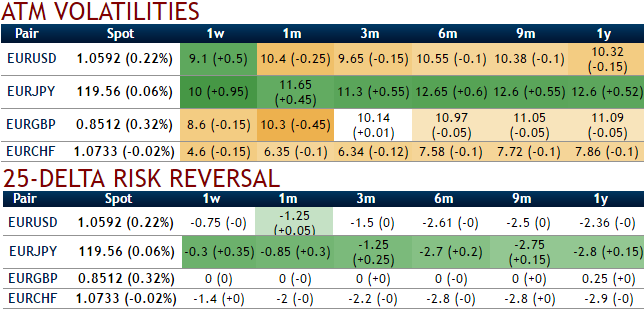

Ahead of today’s Draghi’s speech, 1w IVs of this pair are rising but you could make out from the skewness of the IVs that are active to signify their interest on either of the spot FX moves. While long-term foreign traders firmly destined to hedge the further downside risks. Let’s also observe 1w risk reversals with positive flashes, compare these computations with ongoing rallies of EURJPY, hence, we reckon capitalizing the rallies optimally utilize in option strategy for downside risks.

The ECB used yesterday’s presentation of its semi-annual financial stability report to take the position regarding the referendum in Italy taking place on 4th December. If Matteo Renzi’s proposal of constitutional reform fails, as the polls suggest, there may be early elections – and higher risk premiums for Italian government bonds.

Not only is the ECB concerned that this may cause unrest on the financial markets. The FX market is nervous too. The implied EURUSD volatility for the coming two weeks recently rose to the levels seen during the rather volatile US election night (see above chart).

As a result, ECB Vice-President Vítor Constâncio underlined yesterday that the ECB would react to “shocks” caused by the Italian referendum. That means Italian politics may become decisive for the ECB meeting on 8th December. We expect the ECB to announce an extension of its bonds purchasing program beyond March 2017 at its last meeting of the year.

The implied volatility of ATM contracts for near month expiries of this the pair are reducing below 10.5% which is good for option writers.

While delta risk reversals flashing up progressively with positive numbers (especially in the case of EURUSD and EURJPY) that signify hedging arrangements for upside risks over the period of time.

Hence, considering OTC market reasoning we think upside risks is on the cards, as result we reckon deploying ATM instruments in hedging strategies are worthwhile.