ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis

You could expect the prospects of expansionary fiscal policy in the US under Trump regime that likely drives US interest rates higher and therefore strengthen the dollar further. Trump is also likely to protect US manufacturing in order to generate more and more employment and this could actually narrow US trade deficit.

The Trump presidency will run until 2021 which will be among most inflationary in last few decades and market has already started discounting it, Fed rate has not been an exception, which is likely to rise more than once in 2017 which in turn, yields on US treasuries are surging higher. Also, the US Fed has stepped up monetary policy tightening and had signaled for more tightening in next few policy meet in 2017. This, in turn, is also creating sufficient ground for inflation to rise.

Trump may put a break on long-term interest rates and convince Fed not only to refrain from further interest rates hikes but also to launch another round of long-term treasury debt purchases in case the economy loses momentum, another round of quantitative easing. Further, his proposals to increase spending and cut taxes will fuel economic growth in 2017 and will thus, also prompt Fed to raise interest rates.

The probability of 50-75 bps rate hike during the first half of 2017 while 25-50 bps in the latter half of 2017 is higher according to the current reading of CME Group’s FedWatch tool. This indicates that there is the high level of confidence in the market about the Fed decision to hike interest rate in 2017.

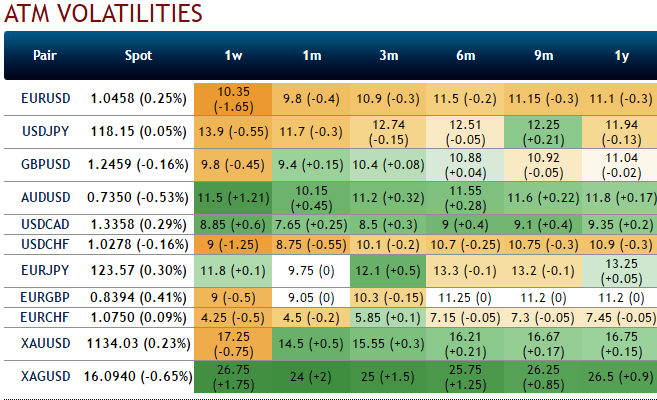

OTC updates:

Please be noted that the IVs of dollar crosses are considerably increasing in longer tenors except EURUSD. As shown in the diagram positively skews in AUDUSD shows the hedgers interests in OTM puts, as a result, we could expect more bearish risks in this pair, while USDCAD has been bullish as the positively skewed IVs signal OTM calls are on more demand comparatively. You could probably understand by now, the impact of Fed’s hints of more hawkish approach in its monetary policy in upcoming meetings.

Well, to understand the volatility construction procedure in FX market strategies, the FX specific delta and ATM conventions knowledge is crucial.

In FX option markets it is common to use the delta to measure the degree of moneyness. Consequently, volatilities are assigned to deltas (for any delta type), rather than strikes. For example, it is common to quote the volatility for an option which has a premium-adjusted delta of 0.25.

These quotes are often provided by market data vendors to their customers. However, the volatility-delta version of the smile is translated by the vendors after using the smile construction procedure discussed below. Other vendors do not provide delta-volatility quotes. In this case, the customers have to employ the smile construction procedure.