Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

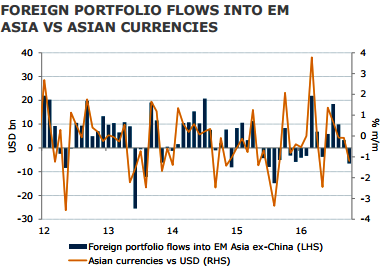

October was the first month since June that total portfolio outflows were recorded.

Though Korean equities managed their eighth straight month of inflows, at USD0.3bn it was not enough to offset the USD3.2bn of outflows from the debt market. Foreign investors have been net sellers of Korean debt for three consecutive months.

Selling had been concentrated in monetary stabilization bonds in October. The outflows contributed to the poor performance of Korean asset prices in the month, with the equity market down 1.7%, 10-year KTB yields rising by over 25bps, and the Korean won depreciating by 3.7% against the USD – making the KRW the worst performing currency in the region.

The BoK left its base rate steady for the fourth straight month at the record low of 1.25 pct at its October meeting, as anticipated.

The EM strategies have turned underweight on Asia FX given a combination of higher core yields, the break out of USDCNY to above 6.70 and multiple idiosyncratic issues. KRW is a notable candidate to short given that it has among the highest sensitivity in Asia to CNY weakness.

The capital outflows from China had already picked up before expectations of a Fed hike and despite resilient data.

The additional dynamic of USD strength and expectations of a Fed hike in December suggests that risks to capital flight are skewed to the upside in Q4.

In addition, the added uncertainty on corporate earnings has the potential to slowdown equity inflows from offshore investors. So, long USDKRW are encouraged at 1135.90 on hedging grounds via 2m NDFs.