S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

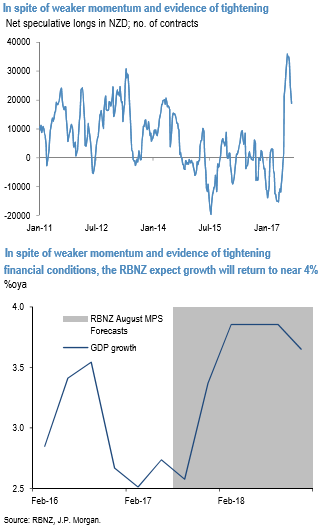

RBNZ is due to release its monetary policy statement tomorrow, wherein it announces OCR rates which is likely to remain on hold. This is going to be the last monetary policy proclamation for the governor, Wheeler in this tenure who has served since September 2012.

Kiwis central bank executives keen onto express desire for a lower currency value. The outgoing Governor stated last week that he “… would have preferred a lower exchange rate” through his term, but caveated this with the comment that “… to a large extent the high exchange rate reflects the favourable performance of the economy, high terms of trade, and weakness in the US dollar.” These comments don’t display much anxiety, but he at least repeated the OCR mantra that “… a lower NZD is needed.

We expect NZD to fall over the next 12 months, as growth will likely continue to underperform the RBNZ’s lofty forecasts (refer above chart), housing slows (refer above chart), and as tight financial conditions restrain any requirement for OCR hikes, allowing rate compression vs USD.

We are also of the view that while systematic/model-based investors might struggle to sell NZD given where the terms of trade are, this is only an anchor for valuations to the extent it predicts growth, inflation, or the current account. On these fronts, we see the details as being less bullish than they appear.

We continue to look for a lower NZD over the coming year, as tight financial conditions, weaker growth, a housing market that has peaked and a policy rate more likely to go down than up in the next year all weigh on the Kiwi. A combination of weaker data and uncertainty ahead of the general election has driven a decent position adjustment in NZD of late (refer above chart), thus, Q4’17 forecasts would be at around - 0.70 and Q2’18 target is at 0.66. Courtesy: JPM

Trade recommendation: Contemplating above aspects, relative-value trades are advised that gives arbitrage investment opportunity that seeks to take advantage of price differentials between FX rates.

Buy NZDUSD straddles of far-month tenors vs shorting AUDUSD 25D strangle, 100:150 vega.