Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

Majority of the Asian markets are shut down for a labor holiday today. Those markets that are open are little changed following modest declines on Wall Street. The oil price is higher with Brent crude close to $75bbl on rising tensions between Israel and Iran. The Australian central bank as expected left interest rates unchanged after its latest policy meeting. Meanwhile, reports suggest that China plans to take a tough stance in trade talks with US officials this week.

Seasonally vol soft April turned out to be anything but soft. The US yield curve’s return to the forefront first in the form of concerns about yield curve flattening and inversion and later on in form of anticipation of the US 10-year breaching the 3% level, a line in the sand. The focus on the yield curve reverberated through FX markets pushing USD vols and JPY cross-vols sharply 0.4-0.5vols higher and sparking a +1.8% broad dollar rally and interest in catch-up bullish USD option prospects.

Overall, over the course of last few days, USD TWI has broken out of the two-month range and has retraced more than half of the January/February drop.

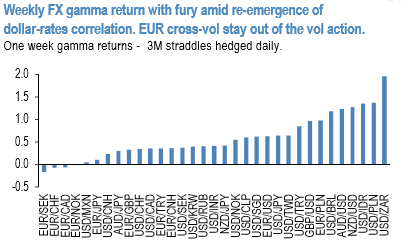

FX gamma returned with fury (refer 1st chart) amid reemergence of dollar-rates correlation and the subsequent FX spot jitters. Predictably, gamma returns concentrated within the USD vols with the high beta heavyweights leading the way. Admittedly, a big chunk of that gamma P/L came from front vols repricing as fears from dollar unwind spread. Amid the market focus on the US yields, EUR cross-vol mostly stayed out of the way of this week vol action.

With technical drivers firmly in the driver’s seat, via the US rates->FX spot->FX vol channel, we turn to assessing current VXY fair value relative to trailing realized USD vols and swaptions instead of taking our more typical approach of regressing VXY on cyclical factors.

Tracking the regression residual, the 2nd chart indicates VXY-Global to be only marginally cheap (0.5 vols) relative to those technical factors based fair value. The tight relationship also implies that absent the USD spot vol and US rates vol drivers, VXY is likely to consolidate. Consequently, we remain reserved about the longevity of the ongoing rates-spot-vol bout but do understand the need and discuss below a few options for hedging of the ongoing market. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: