China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Oil Prices Rise as Hormuz Reopening Remains Uncertain

Oil Prices Rise as Hormuz Reopening Remains Uncertain  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise

US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  S&P 500, Nasdaq Futures Rise as Iran Risks and CPI Loom

S&P 500, Nasdaq Futures Rise as Iran Risks and CPI Loom  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

Canadian data announcements have been lined up for the next weeks, with unemployment data scheduled for today, BoC monetary policy is on 15th followed by press meet, while retails sales and CPI flashes to print on 21st and 22nd respectively.

The market has already lowered its expectations for today’s publication of the Canadian labour market report for March. It expects a loss of half a million jobs and a rise of the unemployment rate by almost 2 percentage points from 5.6% to 7.5%. The US labour market report last Friday gave a first taste of how pronounced the economic collapse in North America has been.

However, similar to the situation in the US the March report in Canada only reflects the data until mid-March.

However, the claims for employment insurance recorded a particularly steep rise from that point onwards: the Canadian government has received 3.18 million requests for income support since 16th March, 2.5 million of which for employment insurance and 642,000 as part of the government’s emergency programme (Canada Emergency Response Benefit, CERB). Even though the government under Justin Trudeau initiated a CAD 71bn. programme as an incentive for companies to keep their employees on the payrolls, according to a poll by the Canadian Federation of Independent Business more than 60% of companies expect lower levels of full time employment over the coming months.

In other words: first of all the market expectations for today’s labour market report might turn out to be too cautious which would put pressure on CAD. Combined with a continued weak oil price that is not a good starting point for the loonie so that USDCAD is likely to remain above 1.3950. However, the real smacker is going to be the labour market report in May as this will then contain the disastrous data from mid-March to mid-April.

OTC Outlook And Options Strategy:

Given these concerns, it makes sense that CAD has decoupled from oil from the recent weeks as the focus on Canada's specific weaknesses grows larger. Despite the move lower in USDCAD this week, we maintain that directionality from here is higher in the pair.

Hence, add longs in USDCAD via options contemplating above fundamental factors and below OTC indications:

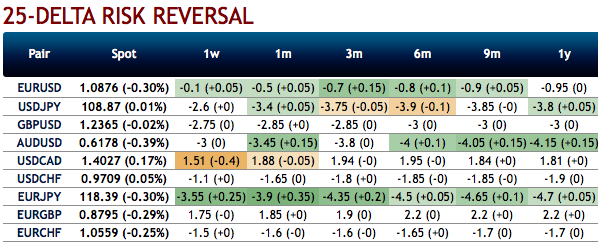

The fresh negative bids are observed to the existing bullish risk reversal setup that indicates the mild price dips amid the broader hedging sentiments for the upside price risks (refer 1st chart).

While the positively skewed IVs of 3m tenors are indicating the upside (refer 2nd chart), bids for deep OTM call strikes up to 1.45 levels is interpreted as the hedgers are inclined for the upside risks.

Hence, at this juncture (when spot reference: 1.4028 levels), we upheld our shorts in CAD on hedging grounds via 3-month (1.3815/1.45) debit call spread. If the scenario outlined above unfolds, we will re-assess our stance but at the moment there are no changes to our CAD recommendations. Courtesy: Sentry, Saxo & Commerzbank