U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

After 3-4 days of bearish streaks in USDMXN, bulls have resumed again in its major bull trend, spiked from the lows of 20.1265 levels to the current 20.6205 levels, rallies continued after Mexican central bank’s monetary policy announcements on Thursday. A lot needs to go right for MXN to get stronger Banxico’s 50bp rate – well expected by consensus and smaller than priced by the market – failed to help the beleaguered peso, which opens up an opportunity to get long USDMXN.

Rate hikes alone will be insufficient to turn around the currency, though more aggressive action could mitigate downside pressure.

As a result, the peso would be on a downward track through to Q1 due to continued pressure on EM currencies as the market adjusts to higher bond yields and a re-rating of Fed expectations coupled with uncertainty regarding Trump’s trade and immigration policies. The 19.9 -20.0 area (previous peak in late September) should offer good support with a move to 23 being our baseline scenario.

Risk premium has fallen, but remains elevated – positioning is still short dollars but has room to increase, MXN is cheap versus oil prices, and implied vol is elevated (though skew has normalized).

However, a lot will need to go right for Mexico (oil, yields, Fed, Trump) to scare away the shorts and the lingering threat of Trump nixing or renegotiating NAFTA prevents a bullish trend from developing.

Brexit and NAFTA are different animals, but price action in GBP could be instructive to understand how the peso might trade – GBP rallies have been limited and shorts positions have been very sticky.

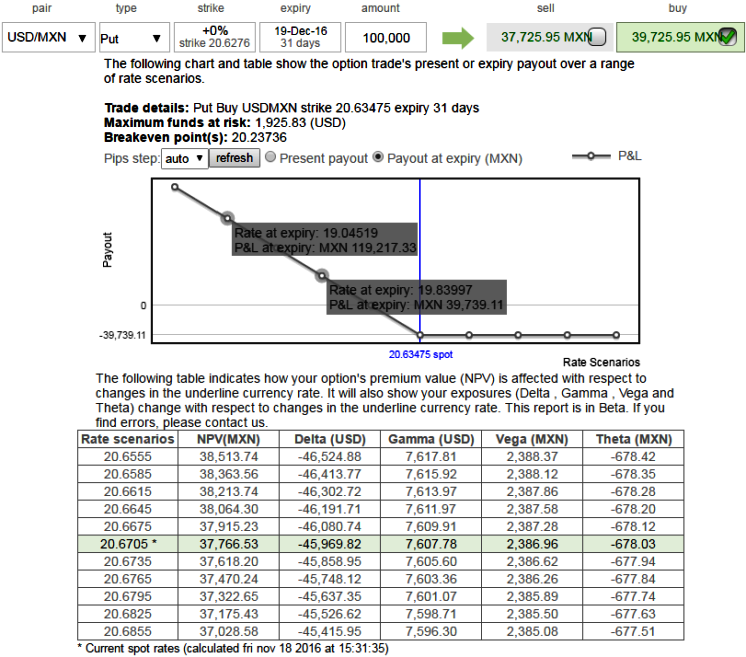

Hence, we encourage longs in USDMXN at spot references of 20.62 for a target at 23.5 and a stop at slightly below the previous peak in late September at 19.8 (-4.0%) but add protective ATM delta puts at the same juncture as the 1w ATM IVs are spiking frantically above 21.6% which is quite conducive for option holders when underlying spot keeps plummeting in next 1weeks’ time; this is quite evident in payoff structure during various underlying rate scenarios.

Elevated volatility argues for a modest initial capital allocation. The time horizon is 3-6 months with negative carry of 40bp/month

Risk profile: (OPEC, Fed, bond yields)

Trump factor, a sustained increase in oil prices could marginally help the MXN; most importantly, watch the November 30th OPEC meeting. Additionally, a turn in bond yields, moderation in Fed tightening expectations, or a marked shift in Trump’s stance toward protectionism would help the MXN.