Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done

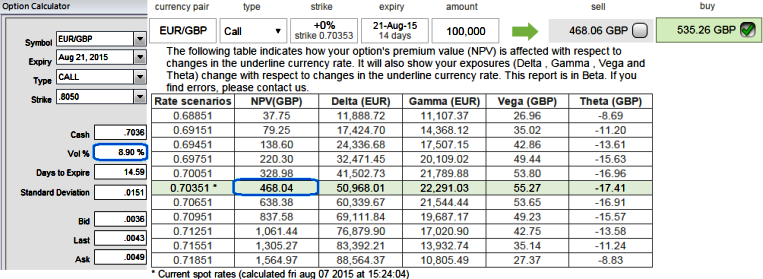

The near month volatility of ATM contracts of this the pair is at 9.15.

Vols of 14D at the money calls - 8.90%

NPV of this call - 468.04 while Premiums trading above 14.36% at GBP 535.26 for lot size 100,000 units.

Hence, comparing this call premium with volatility we think the hedging cost would not be economical as result of deploying ATM instruments.

But we cannot afford to get stuck in this riddle without hedging, so what's the alternative, here comes the strategy arbitrage strategy in which options trading that can be performed for a riskless profit as EURGBP ATM call options are overpriced relative to the underlying exchange rate of EURGBP.

To perform this conversion, the hedger holds the underlying spot FX and offset it with an equivalent synthetic short spot FX (long put + short call) position. Profit is locked in immediately when the conversion is done, the profit would be strike price of call/put - purchase price of underlying + call premium - put premium.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Option arbitrage for EUR/GBP as NPV of ATM calls indicates overpriced premiums

Friday, August 7, 2015 11:15 AM UTC

Editor's Picks

- Market Data

Most Popular