‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  European Stocks Rally on Chinese Growth and Mining Merger Speculation

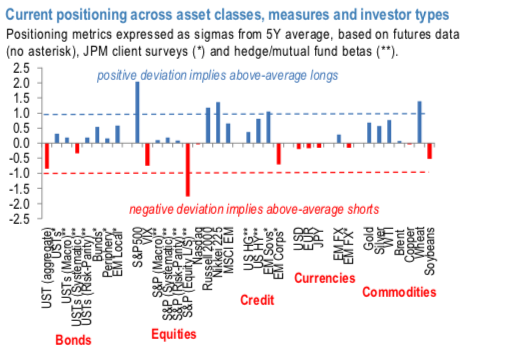

European Stocks Rally on Chinese Growth and Mining Merger Speculation  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

The news of Iranian missile attacks on two US airbases in Iraq caused a sell-off in Asian equities and a rally in safe-haven assets such as government bonds. The Brent crude oil price initially spiked sharply to almost $72bbl but later fell back after Iranian sources said that the country was not looking for war with the US.

Meanwhile, a Boeing 737 bound for Ukraine crashed just after taking off from Iran. However, it has been described as a technical accident, unrelated to the rise in Middle East tensions. In Germany, November factory orders posted a much larger-than-expected decline of 1.3% suggesting that manufacturing’s malaise continues.

US airstrike on Iraq/Iran provocation (unexpected, positive for oil complex, small negative for cyclicals). It’s always debatable whether Gulf politics is any more or less stable in a given year given that intra-regional conflict and US intervention have comingled for decades.

The ‘risk off’ reaction to the latest Middle East news has been relatively muted as markets continue to assume that the situation will not seriously escalate. So although government bonds and other safe-haven assets have rallied, most foreign exchange rates are little changed from yesterday. Energy commodities have taken aback, with WTI crude fell 1.09% to trade at $62.10 and Brent dropped by 0.60% trading at $.67.84 levels a barel.

What does change annually is the oil price’s sensitivity to shocks, depending on whether balances are tight or loose when the flashpoint is triggered and whether investor positioning is long or short of crude. The tighter the market and the shorter the positioning, the greater the scope for large and persistent price gains.

As discussed earlier, positioning has already reversed from short in Q3 (around the time of the drone attack on Saudi facilities) to reasonably long, though more so in WTI than in Brent futures (refer above chart). But the market balance has tightened to a slight deficit (perhaps 200kbd on a 12-mo moving average basis) given OPEC+ over- compliance with supply cuts, which was then formalized through Q1’2020 at the December producers’ summit.

A report by OPEC also indicated that production outside of the cartel may decline in 2020, particularly within the US shale basins, which added further bullishness to the energy commodity market. Hence, we advocated derivatives trades on crude oil, we wish to continue them on hedging grounds.

The strategy reads this way: Maintain longs in CME WTI futures of January’2020 month deliveries. Courtesy: JPM & Commerzbank