Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  BOJ Holds Rates at 1% as Inflation Outlook Eases, October Rate Hike Still Possible

BOJ Holds Rates at 1% as Inflation Outlook Eases, October Rate Hike Still Possible  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

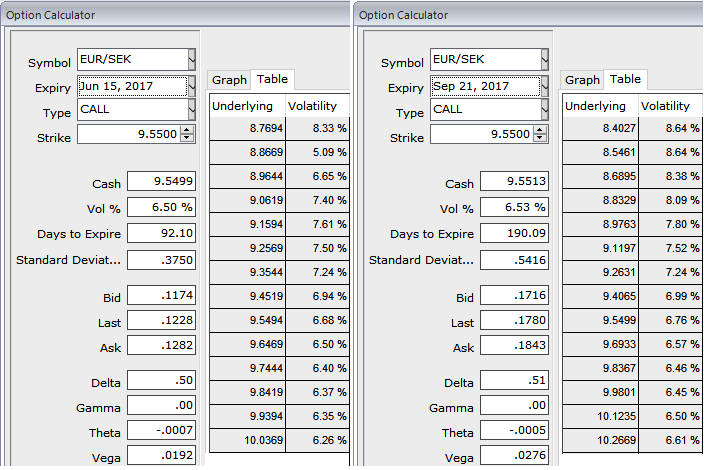

Sell a put against existing cash short in EURSEK. Stay short NZDSEK in options The structural case for SEK appreciation remains intact the real effective exchange rate is 10-11% below its long term average despite an economy that has a positive output gap and which continues to deliver above-trend growth. This week it was reported that Q4’16 GDP jumped by 4.2%.

In addition we upgraded our forecast for Q1’17 from 3.0% to 4.0% (the Riksbank expects 3.2%). The problem for SEK is not the economy but rather monetary policy which is still myopically fixated on delivering at-target core inflation.

A central plank of the central bank’s strategy is too impede a fundamentally justified appreciation in SEK for as long as it can, which is why we expect only a relatively slow pace of SEK appreciation. In order to better reflect the outlook for a slow grind higher in SEK we are converting our cash short in EURSEK into a covered put.

This serves to improve our entry level by around 0.5% and provides some positive time decay as SEK is prone to consolidate in the four weeks between the only data point that matters for Riksbank, CPI. EURSEK vols like all euro pairs are elevated as result of the French election premium so there’s added value in selling lower-strikes in EURSEK at this juncture. 3-mo implied vol of 6.65% compares to realized vol of only 4.9%.

Sell a 3-mo EURSEK put, strike 9.35. Receive 0.52%. Spot reference 9.5533.

Sold EURSEK at 9.4847 on January 13. Stop at 9.6850. Marked at -0.54%.

Bought a 6-mo NZD put/SEK call, strike 6.10 for 1.47%. Spot reference 6.2372. Marked at 0.42%.