Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

The break of 8.0 on USDJPY 1Y ATM vol back in December had caused a frisson of excitement among vol accounts looking to buy Yen vega as a strategic late cycle FX vol play, but what was deemed to be a key technical support level has long since been left in the dust. 7.0 now looms as the next major target, beyond which there is still substantial room to fall to revisit pre-GFC levels in the 6s. It is difficult to argue with option prices steadily softening when the spot is stuck in a tight 109-111 range and delivering 2-2.5 pts. below implieds. There is also a case to be made that the ongoing softness in realized vols can continue longer than some anticipate, since the propensity of the Yen to rally in market downturns is being dampened by a cyclically wide US-Japan interest rate differential that is fuelling above-average equity and FDI outflows, alongside a reduction in FX hedge ratios of traditionally well-hedged foreign bond purchases.

As is almost always the case around this time of the year, such realized vol drags are being exacerbated by drip supply of vega from Japanese importers who are beginning to add to USD-buying FX hedges with embedded short optionality on downticks in USDJPY spot.

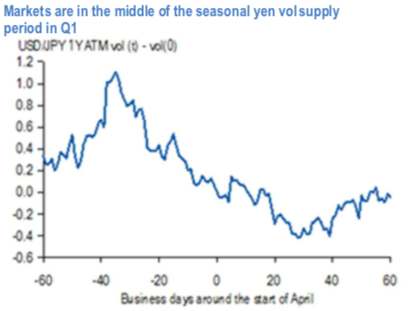

Over the past few years, much of this flow has been well-known to be concentrated in and around the Japanese fiscal new year at the end of March, which imparts a distinct bearish seasonality to the behavior of yen vol in Q1 and early Q2 (refer 1stchart). The magnitude of this seasonal decline is substantial: the average peak-to-trough dip of 1.4 % pts. over a 3-month period centered around March 31stsuggested as shown in 2ndchart that is in excess of 1-sigma of quarterly variability of Yen vol over the past decade. Anecdotal accounts suggest that transactions in such hedges are also turning increasingly tactical i.e. spot USDJPY level dependent, with the result that corporate vega supply, even if in smaller clips outside of the peak months, is becoming something of a persistent feature of the market. While difficult to quantitatively compare with the 2006/07 period in the absence of publicly available transaction data, this corporate flow bears shades of the well-known Uridashi-driven vol supply of the pre-GFC years that had pressured USDJPY 1Y vol to all-time lows in the mid-6s by late 2006.

We are also given to understand that the 2019 vintage hedges have been extremely light so far, implying that the decline in Yen vol YTD has largely been a global macro risk premium compression story with almost no idiosyncratic flow assistance from importers. This, and the fact that we are deep in the middle of the traditional FX hedging season, renders any notion of purchasing Yen vega premature. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index is flashing 0 (which is absolutely neutral), while hourly JPY spot index was at 107 (highly bullish) while articulating (at 05:30 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex