Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

The summary of the BoE meeting in March contained three main triggers for changes to the BoE’s current monetary policy stance.

1. CPI inflation. 2. Wage growth. 3. Private consumption.

• Higher CPI inflation and/or higher wage growth than currently expected would increase the likelihood of a hike.

• Slower private consumption growth than expected would increase the likelihood of a cut.

In line with our expectations, the Bank of England (BoE) made no policy changes at its March meeting and reiterated its neutral stance by repeating it could move ‘in either direction’.

• However, there was a hawkish twist. First, Kristin Forbes (a known hawk) voted for a March hike. Note, though, that she is leaving the BoE on 30 June 2017, which makes her hawkish stance less important. Second, the statement revealed that ‘some members noted that it would take relatively little further upside news…for them to consider that a more immediate reduction in policy support might be warranted’.

• We still expect the BoE to remain on hold for the next 12 months. While we think it is unlikely the BoE will tighten monetary policy in a time of elevated political uncertainty, we think we need to see substantially slower growth and/or higher unemployment before easing becomes likely again. Also, BoE Governor Mark Carney has said that one of the reasons the UK has been resilient to Brexit uncertainties so far is due to the significant monetary easing from the BoE.

• Note that the BoE reaction function has changed since the financial crisis: BoE puts more weight on growth/unemployment relative to inflation.

In our view, the BoE seems to be more worried about slower growth than too-high inflation if this is only temporary.

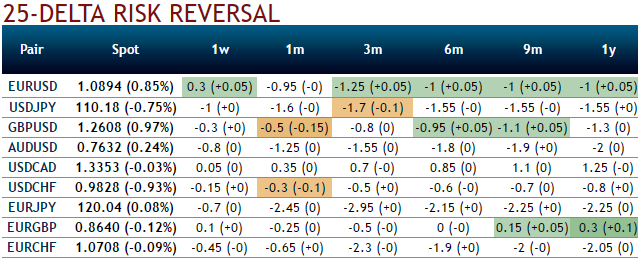

OTC Outlook:

Delta risk reversals of EURGBP: As a result of that macro theme and central bank’s driving forces, from the nutshell showing delta risk reversals of EURGBP, you can probably make out that the pair has been one of the most expensive pairs to be hedged for upside risks as it indicates calls have been relatively costlier over puts but hedging sentiments for upside risks are intensified in 1 year tenor.

Needless to specify, GBP vols have still been flying high pace no matter what both prior and post-Brexit events, but this time these IVs are also owing to BOE’s monetary policy decision.