Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue

Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue  Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease

Gold Prices Surge 7% as Dollar Falls, Fed Rate Hike Bets Ease  Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data

Asian Stocks Mixed as Chip Selloff Hits KOSPI, Nikkei Ahead of US Jobs Data  Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan

Asian Stocks Slide as Semiconductor Selloff Weighs on South Korea and Japan  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade  Gold Prices Steady as Hormuz Tensions Fuel Fed Rate Concerns

Gold Prices Steady as Hormuz Tensions Fuel Fed Rate Concerns  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  Oil Prices Set for Steep Weekly Losses as Hormuz Deal Stalls

Oil Prices Set for Steep Weekly Losses as Hormuz Deal Stalls  US Dollar Falls as Weak July Jobs Report Dents Fed Rate Hike Bets

US Dollar Falls as Weak July Jobs Report Dents Fed Rate Hike Bets  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

January’s manufacturing PMI dipped to 55.9 from 56.1 in December, exactly in line with both our and consensus expectations. Despite the mild dip, the headline balance remains well above its historic average of 51.6 and the average over 2016 Q4 of 54.8.

The details of the report show that both export and domestic orders continue to expand, although the strength of exports seems particularly underwhelming despite the 12% post-referendum drop in sterling’s effective exchange rate. In fact, the export orders balance fell to 50.9 – barely above its historic average – from 55.6 last month. Currency weakness meanwhile continues to feed through to costs. The input price balance rose to 88.3, the highest on record, with prices charged also accelerating to 63.7, again one of the highest-ever readings.

Taken at face value, the elevated level of the PMI suggests that the contribution of manufacturing to UK GDP growth in 2017 is likely to be more positive than in recent months, despite the divergence of official estimates and surveys of activity since the referendum. That message is reinforced by the future expectations balance newly introduced in this release, which at 72.5 is at an 8-month high and well above the 50 no-change mark.

As the manufacturing sector accounts for only around 10% of UK economic activity, the UK’s growth outlook will nevertheless be primarily driven by the dominant services sector.

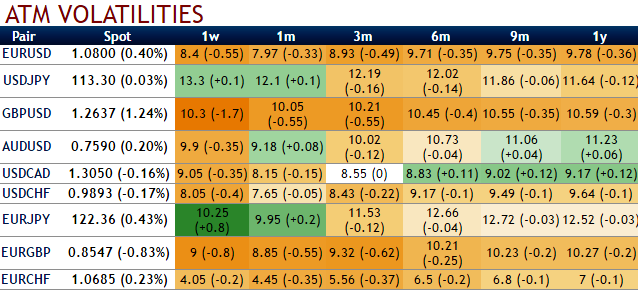

Please be noted that the reducing IVs for GBPUSD and EURGBP despite the flurry of significant economic news:

Fed’s funds rate which is likely to be announced shortly, the services PMI for UK due on Friday – coming after the Bank of England’s policy decision on Thursday, but with a preview seen by the MPC – is still expected to be at a level consistent with little slowdown from the 0.6% q/q GDP growth pace estimated for 2016 Q4. Whether service sector growth remains robust in the course of 2017 is a key issue for this year: the drag of rising prices on consumer purchasing power will be a key area to watch.