Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise

EURSEK is unchanged over the past month, albeit once again the cross briefly flirted with the upper end of the six-year range at 9.60-9.70.

We expect continued range-trading through until year-end and then only very modest appreciation from SEK through next year (9.35 by end-16 and 9.15 by Q3’17).

The catalyst for a major break higher in SEK is lacking – a definitive end to the Riksbank easing cycle and a tangible prospect of rate hikes within a 6-9 month time frame.

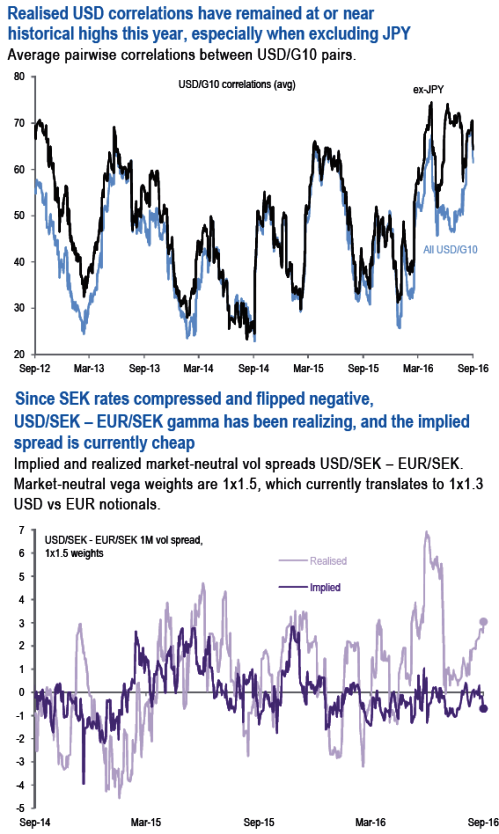

In the case of SEK, long positions in USD vols can be advantageously coupled with short vols in the EUR cross.

Long gone are the days when the market was testing the Riksbank’s nerves in the low 9.0s in EURSEK. The latest Swedish data do point to a rebound from slowing economic momentum.

However, this did very little to improve sentiment and lift SEK, as the undershoot in the country’s Economic Activity Surprise Index (EASI) is second only to NZD among the pairs we track .

With the market looking for negative rates to extend to Q3 2019 – a good 1y past the Riksbank’s forward guidance, it is unlikely that SEK attracts significant inflows, and “we expect continued (EURSEK) range-trading through until year-end”. This range-bound outlook on EURSEK – which the price action around German.

Financials woe doesn’t question, should play its part in keeping USD correlations at historically firm levels, especially when removing the BoJ-led effect of JPY. It is, therefore, supportive of a USDSEK vs EURSEK vol spread trade.