J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

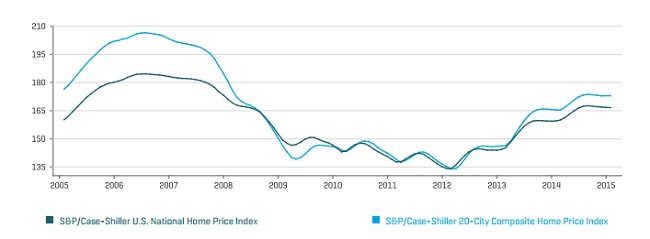

Yesterday S&P/Case-Shiller home prices were released in US, that showed housing market is still far from recovery and might not be strong enough to handle rate hikes by FED.

- US mortgage rates, especially the fixed rates have risen already in anticipation of rate hike by US Federal Reserve this year.

- While 30 year yield has to lend to US governments has been close to 2.5%, people are paying around 3.6%-4% for 30 year tenure prime mortgage. However Mortgage rates have somewhat eased 30 to 40 basis points from last year's high in 2014.

Chart attached explains home prices as measured by S&P/Case-Shiller index for national and 20 cities. S&P/Case-Shiller index is based on pioneering research of Robert Shiller and Karl Case, which tracks real estate prices across nations and generally considered as a leading indicator.

Latest reading shows further softening of home prices across nation.

- Index fell nationwide by -0.06%, whereas top 20 cities saw drawdown of -0.03% on monthly basis.

FED this year facing several hurdles to decide on rate hike mainly from weaker manufacturing and housing. Reports suggest that people are facing trouble to refinance their mortgages.

Weaker data from housing sector will continue to pose challenge for FED to decide on suitable rate hike path. Moreover, Charles Evans group might increase inside FOMC, who are calling for first rate hike in 2016.