Dollar Slides as Softer US Inflation Dims Fed Rate Hike Expectations

Dollar Slides as Softer US Inflation Dims Fed Rate Hike Expectations  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  China Q2 2026 GDP Misses Forecast as Weak Domestic Demand Offsets Export Strength

China Q2 2026 GDP Misses Forecast as Weak Domestic Demand Offsets Export Strength  China Trade Surplus Hits $125.6 Billion as June Exports, Imports Smash Forecasts

China Trade Surplus Hits $125.6 Billion as June Exports, Imports Smash Forecasts  Australia Consumer Sentiment Rises in July as Fuel Price Relief Lifts Confidence

Australia Consumer Sentiment Rises in July as Fuel Price Relief Lifts Confidence  ECB's Kocher Says No Inflation Spillover Yet From Iran Conflict, Warns Risks Remain

ECB's Kocher Says No Inflation Spillover Yet From Iran Conflict, Warns Risks Remain  Goldman Sees Foreign Investors Driving India Stock Market Recovery

Goldman Sees Foreign Investors Driving India Stock Market Recovery  Oil Prices Climb as Trump Escalates Iran Pressure, Strait of Hormuz Risks Grow

Oil Prices Climb as Trump Escalates Iran Pressure, Strait of Hormuz Risks Grow

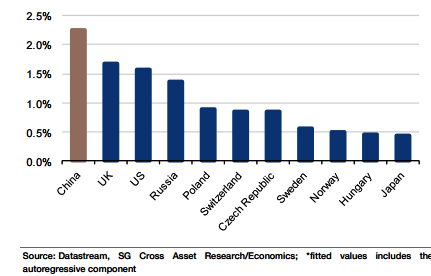

The pass-through of a weaker euro (which depreciated 10% between July 2014 and July 2015) so far can only be traced to the early stages of the price chain, i.e. import prices growth has gone from -1% to 1.8% yoy during the same period.

The impact of a weaker euro has not yet shown any pass-through to domestic producer prices for accelerated growth in HICP non-energy industrial goods prices.

"Despite an increase in import prices with the weaker euro, producer prices (excluding construction and energy) have shown no sign of quickening, suggesting that companies have either reduced profit margins by not raising output prices or that windfall gains from lower energy prices may have helped them keep producer prices low", says Societe Generale.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Impact of weaker euro visible but only on import prices

Wednesday, September 23, 2015 3:18 AM UTC

Editor's Picks

- Market Data

Most Popular