Oil Prices Steady as U.S.-Iran Truce Uncertainty and Middle East Tensions Keep Markets on Edge

Oil Prices Steady as U.S.-Iran Truce Uncertainty and Middle East Tensions Keep Markets on Edge  German Auto Suppliers Turn Bearish as Investment and Jobs Shift Overseas

German Auto Suppliers Turn Bearish as Investment and Jobs Shift Overseas  Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks

Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks  Trump Says No Hormuz Strait Tolls During 60-Day Iran Ceasefire

Trump Says No Hormuz Strait Tolls During 60-Day Iran Ceasefire  Australia Eases Capital Gains Tax Reforms to Support Small Businesses and Startups

Australia Eases Capital Gains Tax Reforms to Support Small Businesses and Startups  Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention

Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention  Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback

Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback  Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns

Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns  US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge

US Stock Futures Slip After Wall Street Rally Fueled by US-Iran Deal and Chipmaker Surge

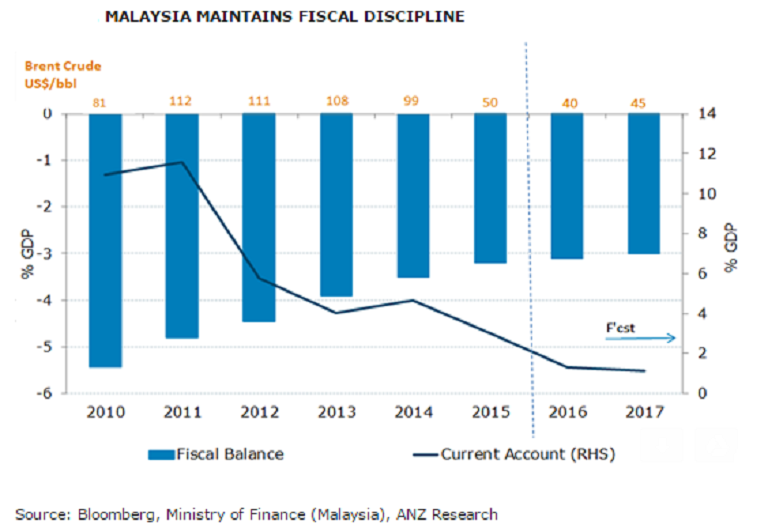

The Malaysian government underlined their commitment to fiscal consolidation when they unveiled Budget 2017 last week. Cutbacks to spending for this year were outlined to keep the fiscal deficit at 3.1 percent of the gross domestic product (GDP) in 2016, with a slight improvement to 3.0 percent in 2017 forecast.

This display of fiscal discipline puts Malaysia’s sovereign credit rating of A- (stable outlook) on a firm footing, particularly with the diversification of its revenue base away from oil. Given that Budget 2017 is supportive of private consumption, Bank Negara Malaysia (BNM) is expected to leave the overnight policy rate unchanged at 3.00 percent at the final meeting of the year on November 23.

Also, the ringgit has underperformed, below market expectations. MYR’s weakness is notable in light of the rebound in oil prices. Despite expectations of rebound in oil prices that prices will stay above USD50/bbl, the near-term outlook for the MYR remains challenging, ANZ reported.

Further, the narrowing in the current account surplus provides less support for the ringgit. US monetary policy normalization and a steeper yield curve in the major developed markets will result in more volatile capital flows.

"For now, we maintain our year-end USD/MYR forecast at 4.15, as we look for some near-term retracement. But the risk is clearly tilted towards further ringgit weakness," ANZ commented in its latest research report.