Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Goldman Sachs Sees US Stock Buybacks Outpacing Equity Issuance as AI Funding Rises

Goldman Sachs Sees US Stock Buybacks Outpacing Equity Issuance as AI Funding Rises  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  European Stocks Flat as Oil Prices Rise, US CPI in Focus

European Stocks Flat as Oil Prices Rise, US CPI in Focus

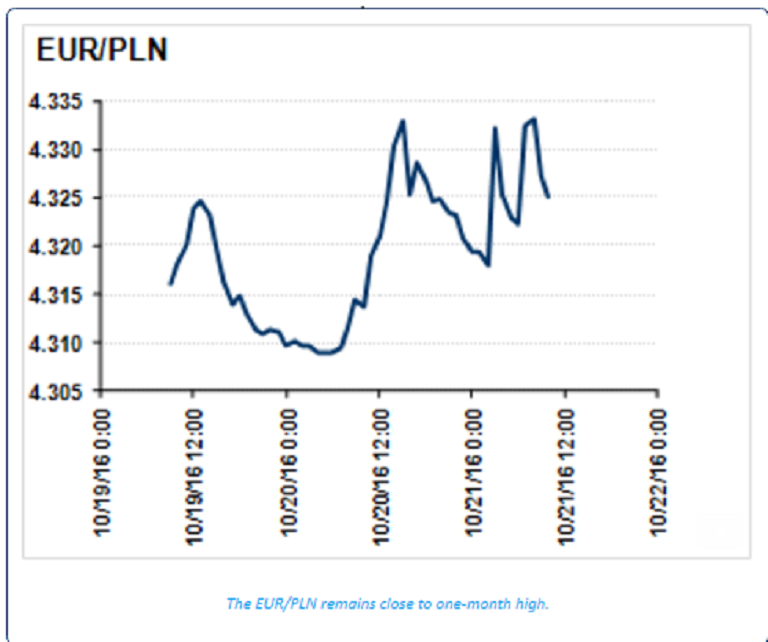

The National Bank of Poland’s (NBP) monetary policy committee (MPC) still sees stable rates as the most likely scenario in the recently released minutes of the latest monetary policy meeting. This is despite the fact that the economic growth will likely be somehow slower than had originally been anticipated.

The stability of the Polish official rates in 2017 remains the base case scenario as well. Still, the zloty weakened against the euro by about 0.5 percent during the day. In the meantime, the Czech koruna remains glued to the Czech National Bank’s (CNB) intervention floor (EUR/CZK 27.0) while EUR/CZK forwards have fallen considerably over the past few weeks as markets prepare on the exit from interventions.

From the point of view of the timing of the exit, yesterday’s meeting of the European Central Bank (ECB) did not bring substantially new information. It is, however, important to keep in mind that the CNB is currently preparing its new economic projection that will be released on November 3 in which the CNB assumes the ECB will terminate its QE programme at the end of March (with no tapering).

Therefore, should the ECB eventually (i.e. at December’s meeting) extend the QE (which cannot be ruled out), this would mean that the exit may also be postponed towards the end of next year, KBC Central European Daily reported.