Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done

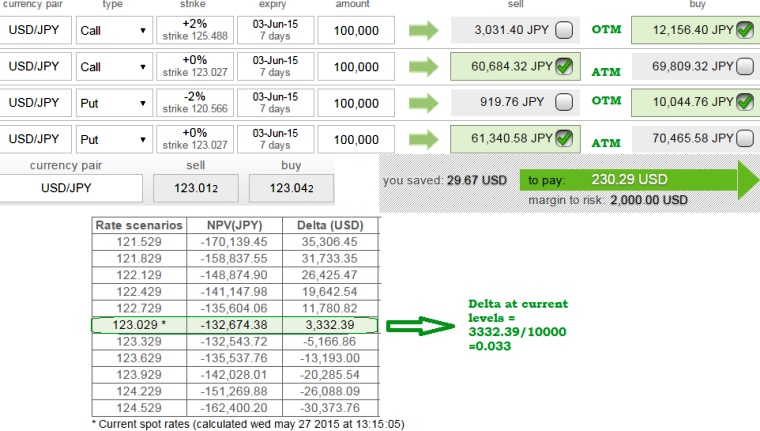

The rate of change option portfolio to a relative change in the spot market price of the underlying currency is shown as below:

For instance in our earlier post we had advocated iron butterfly, where ATM Call & Put were sold and simultaneously OTM Call & Put were bought on this pair.

Let's just revisit on this portfolio that was built earlier:

The OTM call has now at current a delta of 0.10 and the price of the underlying goes up by $0.0004, the value of the call could be expected to go up by approximately $0.0002.

While ATM call, delta approaches 0.50.

The OTM put has now at current levels a delta of 0.89, so any smaller change in the market price of the underlying will produce very little change in the value of the put.

If a put has a delta of 0.5 and the price of the underlying goes down by $0.0002, the value of the put could be expected to go up by approximately $0.0001.

As a whole, the strategy has been nearing delta at zero (accurately at 0.03) as shown in the figure.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Portfolio analysis on Iron butterfly USD/JPY

Wednesday, May 27, 2015 8:05 AM UTC

Editor's Picks

- Market Data

Most Popular