Trump Threatens Higher Canada Tariffs as Wildfire Smoke Sparks U.S. Air Quality Crisis

Trump Threatens Higher Canada Tariffs as Wildfire Smoke Sparks U.S. Air Quality Crisis  Wall Street Ends Lower as AI Selloff, Iran Tensions Weigh on Tech Stocks

Wall Street Ends Lower as AI Selloff, Iran Tensions Weigh on Tech Stocks  Deutsche Bank Says Fed Balance Sheet Cuts Could Weaken US Dollar Instead of Boosting It

Deutsche Bank Says Fed Balance Sheet Cuts Could Weaken US Dollar Instead of Boosting It  KB Securities Explains Why KOSPI Is Falling Despite Strong Samsung, SK Hynix Earnings

KB Securities Explains Why KOSPI Is Falling Despite Strong Samsung, SK Hynix Earnings  Asian Stocks Rise as Oil Retreats on Iran Ceasefire Hopes Ahead of Key AI Earnings

Asian Stocks Rise as Oil Retreats on Iran Ceasefire Hopes Ahead of Key AI Earnings  AI Chip Stocks Face Valuation Pressure as Investors Shift Toward Big Tech and Software

AI Chip Stocks Face Valuation Pressure as Investors Shift Toward Big Tech and Software  Nikkei Plunges 5% as AI Stock Selloff Spreads Across Asia

Nikkei Plunges 5% as AI Stock Selloff Spreads Across Asia  Malaysia Q2 Economy Grows 5.8%, Beating Forecasts on Strong Tech Exports and Domestic Demand

Malaysia Q2 Economy Grows 5.8%, Beating Forecasts on Strong Tech Exports and Domestic Demand  US-Iran Conflict Escalates as Gulf Attacks Threaten Global Oil Supply

US-Iran Conflict Escalates as Gulf Attacks Threaten Global Oil Supply  Gold Climbs Above $4,000 as Middle East Tensions and Fed Outlook Drive Safe-Haven Demand

Gold Climbs Above $4,000 as Middle East Tensions and Fed Outlook Drive Safe-Haven Demand  Brent Oil Jumps 16% for Best Week Since April as US-Iran Conflict Fuels Supply Fears

Brent Oil Jumps 16% for Best Week Since April as US-Iran Conflict Fuels Supply Fears  ASEAN Ministers Warn Middle East Conflict Threatens Regional Stability and Energy Security

ASEAN Ministers Warn Middle East Conflict Threatens Regional Stability and Energy Security  US Stock Futures Hold Steady as Tesla, Alphabet Earnings and Iran Conflict Dominate Market Focus

US Stock Futures Hold Steady as Tesla, Alphabet Earnings and Iran Conflict Dominate Market Focus  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  US Stock Futures Rise as AI Optimism Lifts Tech, 3M Jumps on Strong Earnings

US Stock Futures Rise as AI Optimism Lifts Tech, 3M Jumps on Strong Earnings  Japan Core Inflation Seen Rising in June, Strengthening BOJ Rate Hike Outlook

Japan Core Inflation Seen Rising in June, Strengthening BOJ Rate Hike Outlook  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

It’s been more than a year since the UK economy was thrown into crisis after then-prime minister Liz Truss suggested making a wealth of unfunded tax cuts in her September 2022 mini-budget. But a recent bond market sell-off has now sent borrowing costs rocketing again, pushing the bond market even higher than after Truss’s announcement.

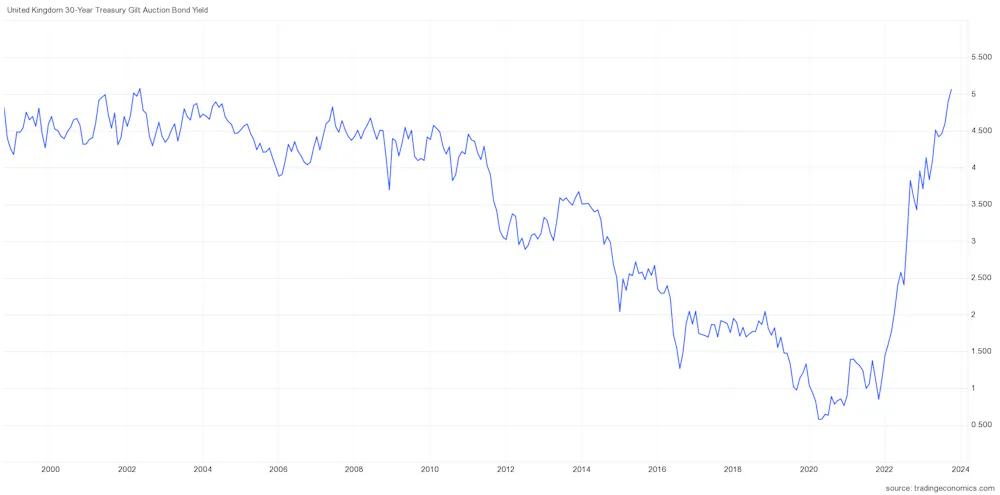

Yields on UK treasury bonds – the rate the UK government must pay to borrow money – have risen to approximately 4.6% for ten-year bonds. Yields on 30-year bonds hit 5.1%, the highest since 1998.

Banks also use this rate as a key benchmark to set commercial loan rates, so this means borrowing costs are rising for businesses, as well as for the government. Two-year and five-year treasury yields (which are used to set mortgage rates) are also above the budget-fuelled high of last year, and at levels not seen in over ten years.

UK bond yields (30 year), 1998-2023:

The government issues treasury bonds at a particular interest rate that corresponds to a fixed value. Investors buy the bonds and the government uses the money to finance its spending. Since it’s a loan, the government repays the investors but also pays interest on the bond until repayment – this is the yield.

For example, a 5% bond issued for a £100 earns the investor £5 interest. If the government issues a later bond at 6% for £100 (£6 interest), the 5% (£5) bond’s value drops. This is why when bond prices fall, the yield rises and vice versa.

Right now, UK treasury yields are rising because investors are trying to sell UK government bonds – falling demand makes the price drop.

And this isn’t just happening in the UK. The same is true around the world. US bonds, for example, recently hit a 16-year high.

Why is this happening right now?

This is a tale of two central banks navigating difficult economic conditions. In September, both the Bank of England and the Federal Reserve chose not to increase their main interest rates (which are at 5.25% and 5.5% respectively). The reasons for these decisions and the position of each economy are driving the bond market changes.

In terms of the economy, headline inflation is currently 6.7% (6.2% for core, which strips out more volatile items like energy) in the UK, and 3.7% (4.3% core) in the US. GDP growth is at 0.6% for the UK and 2.4% for US. So, the two economies are on different tracks.

These figures influence financial market expectations about what central banks might do next with interest rates. The divergence in growth rates and inflation between the two economies had signalled that the banks would take different routes at their September meetings.

Prior to the latest decision by the Bank of England, there was a general view that UK rates would rise to 5.5%, but a lower-than-expected inflation rate was announced days before the bank met to decide on rates and this led them to hold rates instead. After the meeting, the Bank of England also indicated that, while it expected its rate to remain at 5.25% for some time, it did not foresee a further rise.

In contract, while the Federal Reserve also held rates in September, this was seen as a pause and not a stop. US rates are widely expected to rise again this year.

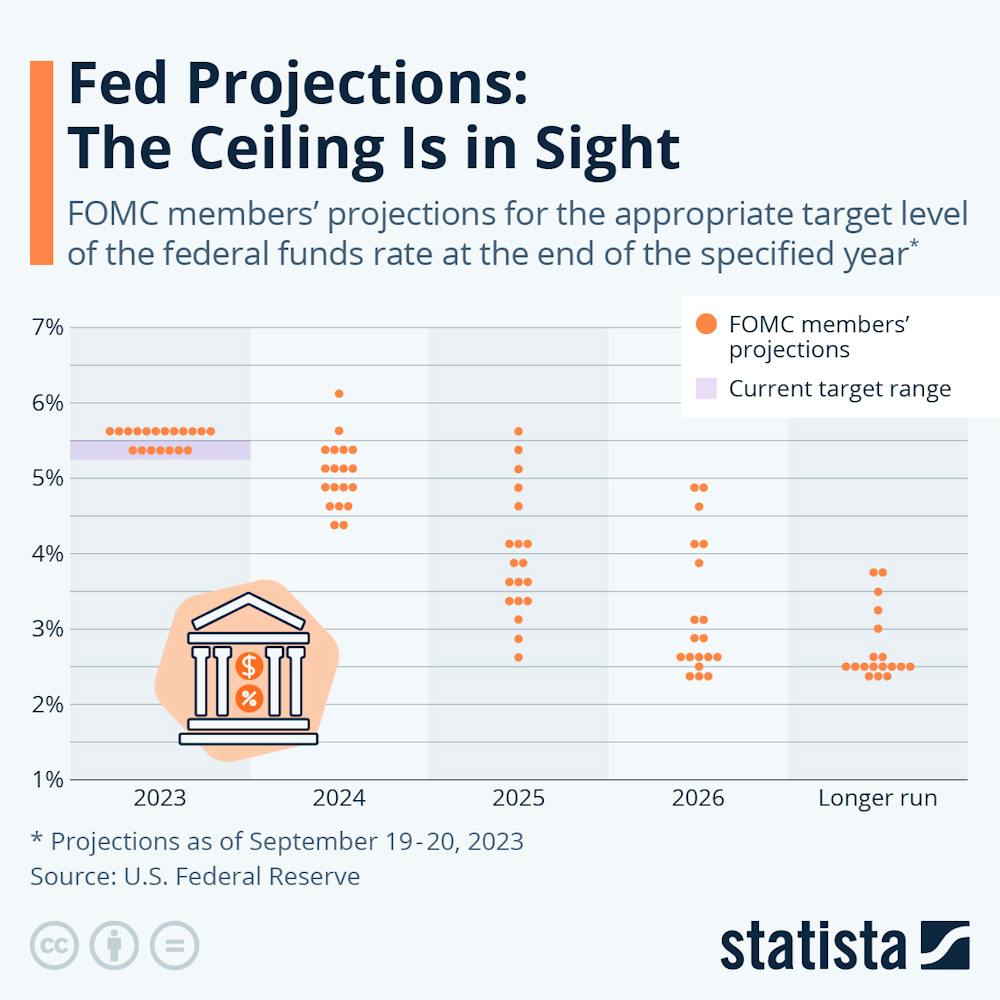

Twelve members of the Fed’s 19-person rate-setting committee expect one more 0.25% interest rate hike this year, while 7 FOMC members expect no change before the end of the year. Statista, CC BY-ND

What has this got to do with bond yields?

The expected rise in US rates means investors do not want to hold US bonds whose value will fall as a result. As explained before, when newer bonds are issued at higher yields (to reflect the bank’s most recent interest rate decison), existing bonds (those previously issued with lower yields) will be valued less by investors because they will get less in interest payments for holding them.

This is why investors are selling US bonds. For a related, but slightly different reason, investors also don’t want to hold UK bonds. As US bonds will soon earn a higher yield, investors are selling UK bonds to reposition their portfolios towards the US, where they will be able to earn a higher yield.

This also has implications for the value of the pound. Since the Bank of England’s decision not to raise the interest rate in September, the value of the pound has fallen versus the US dollar. This is because the same investors that are selling UK Treasuries and driving up yields, are also selling pounds to buy US dollars.

The UK is not alone in feeling this effect, the euro is also weakening and against the US dollar, while the Japanese yen is close to the same low that prompted an intervention by the Bank of Japan around this time last year.

Global currency markets. Dilok Klaisataporn/Shutterstock

In each case, the reason is the same: the strength of the US economy relative to other economies (0.5% GDP growth for the Eurozone and 1.6% for Japan) is attracting more investors. As with the UK, the policy rates for the Eurozone and Japan are below those of the US, with each central bank indicating an intention not to make further increases.

But both of these effects – higher treasury yields and a depreciating pound – spell bad news for the UK economy.

The higher yields imply higher borrowing costs, including interest payments for the government, as well as both mortgages and business loans. The fall in the value of the pound means that imports are more expensive. Together with the fact that many commodities (such as oil) are priced in US dollars, this can contribute to higher inflation.

Since the economy is also barely growing, both issues will continue to have a dampening effect on the UK.

David McMillan does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.