Wall Street Ends Lower as AI Selloff, Iran Tensions Weigh on Tech Stocks

Wall Street Ends Lower as AI Selloff, Iran Tensions Weigh on Tech Stocks  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  Asian Markets Cautious as Oil Tops $90, AI Earnings and Fed Rate Fears Weigh on Sentiment

Asian Markets Cautious as Oil Tops $90, AI Earnings and Fed Rate Fears Weigh on Sentiment  Asian Currencies Hold Steady as Middle East Tensions Boost US Dollar, Oil Concerns

Asian Currencies Hold Steady as Middle East Tensions Boost US Dollar, Oil Concerns  US Dollar Holds Near One-Week High as Middle East Tensions and Oil Prices Drive Market Sentiment

US Dollar Holds Near One-Week High as Middle East Tensions and Oil Prices Drive Market Sentiment  AI Chip Stocks Face Valuation Pressure as Investors Shift Toward Big Tech and Software

AI Chip Stocks Face Valuation Pressure as Investors Shift Toward Big Tech and Software  Germany Producer Prices Rise 1.8% in June, Missing Forecasts

Germany Producer Prices Rise 1.8% in June, Missing Forecasts  Brent Oil Jumps 16% for Best Week Since April as US-Iran Conflict Fuels Supply Fears

Brent Oil Jumps 16% for Best Week Since April as US-Iran Conflict Fuels Supply Fears  Gold Climbs Above $4,000 as Middle East Tensions and Fed Outlook Drive Safe-Haven Demand

Gold Climbs Above $4,000 as Middle East Tensions and Fed Outlook Drive Safe-Haven Demand

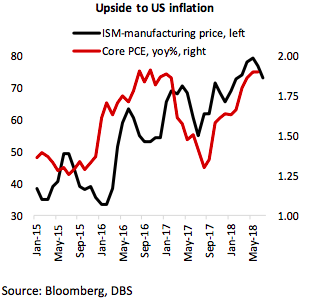

The United States’ annual real gross domestic product (GDP) is expected to grow by 3 percent, while inflation (as measured by the US Urban Consumers CPI) to average around 2.5 percent, according to the latest report from DBS Group Research.

Surveys of businesses show both uncertainty about the outlook and the beginning of a trend of earnings projections being revised downward (starting with automobile manufacturers). But there are broader, still-supportive dynamics at play.

Last year’s tax cut will act as a shock absorber to potential downside from tariff wars, consumer spending is healthy, labour market is tight, fiscal stance is growth supportive, and trade, despite the poor headlines, is still robust, the report added.

This path of economic data would not only ensure that the US Federal Reserve hikes two more times this year, but a continuation of the quarterly rate hikes can be expected next year as well. Inflation upside is likely (especially if trade wars continue and US-Iran conflict takes place), but so far the markers are modest, causing no heightening of concern for Fed policy.